Table of Contents

Overview of March 2026 Rate Super Week

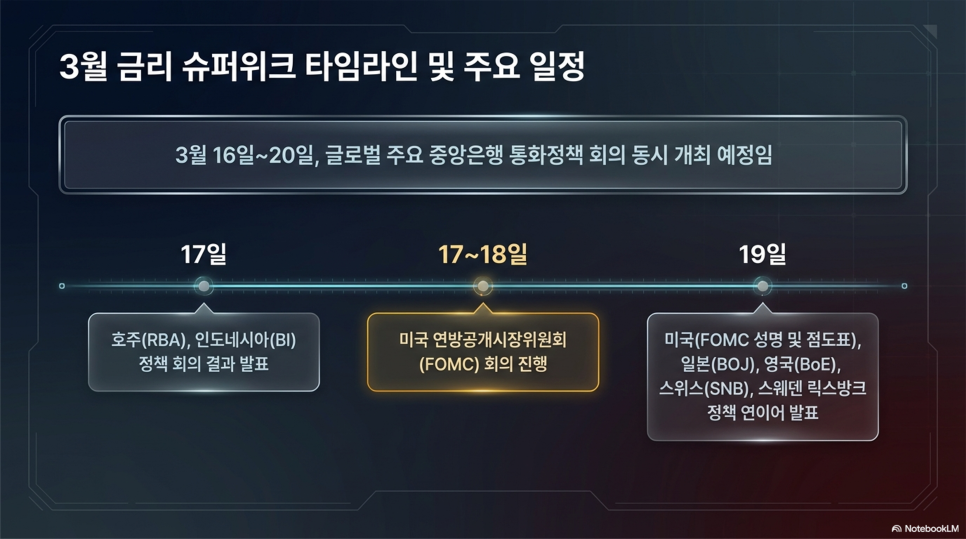

The week of March 16 to 20 is a critical moment for global financial markets, as many major central banks are conducting monetary policy meetings simultaneously. This period is commonly referred to as "Rate Decision Super Week."

The key schedule is as follows.

March 17

The announcement of the cash rate by the Reserve Bank of Australia (RBA) will take place at 12:30 PM Korean time.

Additionally, the results of the meeting of Bank Indonesia (BI) will also be announced.

March 17-18

Meeting of the US Federal Open Market Committee (FOMC)

March 19

The FOMC statement will be released at 03:00 Korean time, followed by a press conference by Chairman Powell at 03:30.

The Bank of Japan and the Bank of England will also implement policy decisions and interest rate announcements respectively.

The Swiss National Bank and the Swedish Riksbank also have important announcements related to interest rates planned.

A key point to note in this meeting is that the US FOMC will announce its quarterly outlook and dot plot. This goes beyond simply freezing or lowering interest rates and is seen as a crucial opportunity to reveal insights into the central bank's future interest rate path. For this reason, this meeting is likely to have a significant impact on the market.

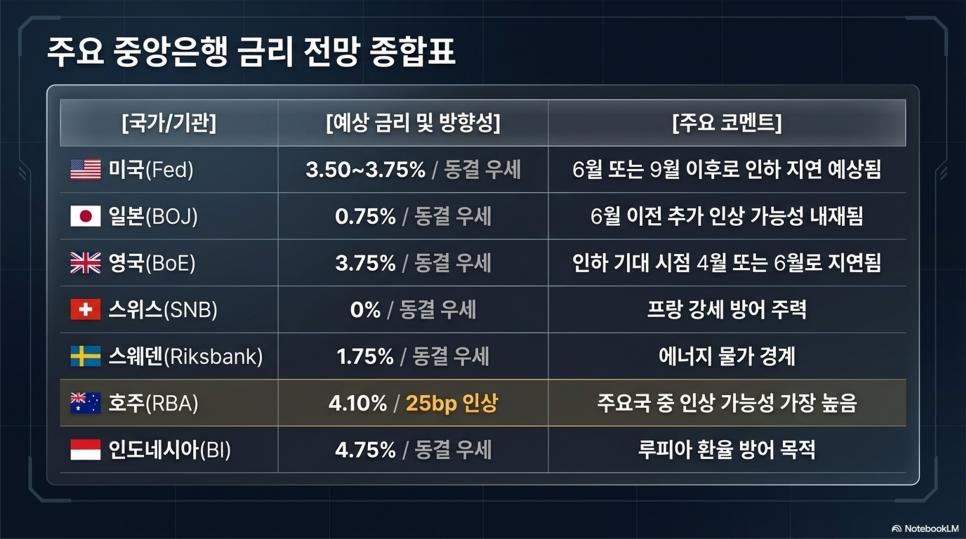

Central Bank Interest Rate Outlook

Looking at the general opinion in the market right now, many central banks are expected to hold interest rates steady. However, some countries show differences in policy direction.

The major outlooks are as follows.

US Federal Reserve (Fed)

The key interest rate is expected to be maintained at 3.50–3.75%.

The market's expected first timing for a rate cut is in June, although some investment banks predict it may be after September.

Particularly, concerns about the resurgence of inflation due to rising oil prices from the war in the Middle East have been raised again.

Bank of Japan (BOJ)

The policy interest rate is expected to remain at 0.75%. However, the possibility of additional rate hikes before June is already reflected in the market.

Bank of England (BoE)

The key interest rate is expected to be maintained at 3.75%. Expectations for the timing of a rate cut are changing, and what was initially expected in March has now been pushed back to April or June.

Swiss National Bank (SNB)

Policy rate

Expected to be frozen at 0%

Managing the strength of the Franc

is currently more important than inflation.

Swedish Riksbank

Policy rate

Expected to be frozen at 1.75%

Reserve Bank of Australia (RBA)

Next week, a central bank likely to raise rates is under focus. The current rate is 3.85%, and it is expected to rise to 4.10% with a 25bp hike.

Bank Indonesia (BI)

Policy rate

Expected to be frozen at 4.75%

Main challenge:

Defending the Rupiah exchange rate

Current Global Macroeconomic Situation

This central bank meeting reflects the uncertain macro environment of the global economy. Due to this situation, the outcomes of this meeting are receiving much attention.

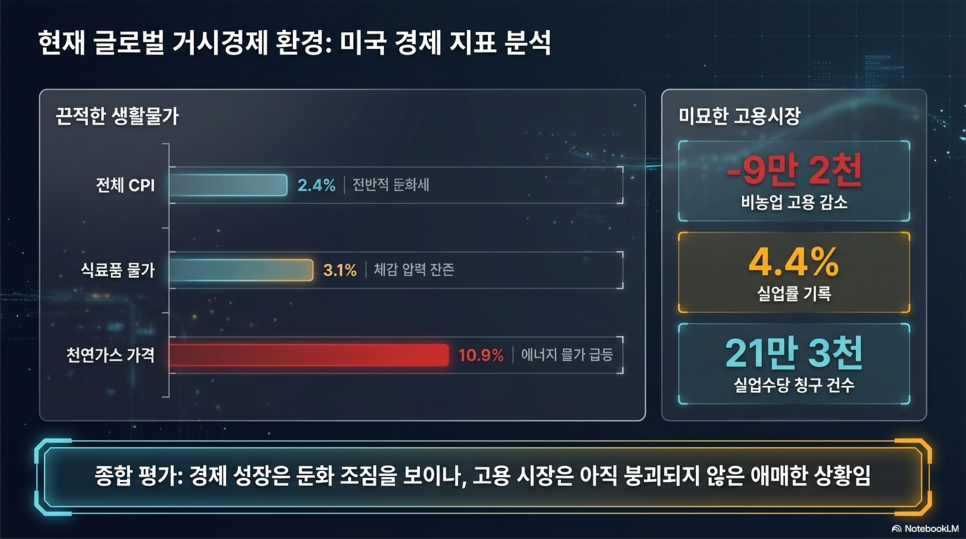

US Economic Situation

Recent US economic indicators show that the Consumer Price Index (CPI) has increased by 2.4%, with the core CPI standing at 2.5%. Food prices have risen by 3.1%, and natural gas prices have increased by 10.9%. Overall inflation is easing, but pressure on living costs still persists.

The labor market also presents a complicated picture. Non-farm employment has declined by 92,000, while the unemployment rate has reached 4.4%. New jobless claims have totaled 213,000. Thus, while the US economy is slowing in growth, the labor market has not yet experienced significant collapse.

Energy Market Variables

Currently, the most significant factor affecting central bank policy is the surge in energy prices resulting from the war in the Middle East.

Recent trends indicate that Brent crude oil prices are projected at $95 per barrel, while gasoline prices in the US have increased by over 20%.

This situation has led the financial market to raise concerns about the possibility of "energy-induced re-inflation."

Monetary Policy Pressures by Country

The monetary policy situations in various countries are slightly different.

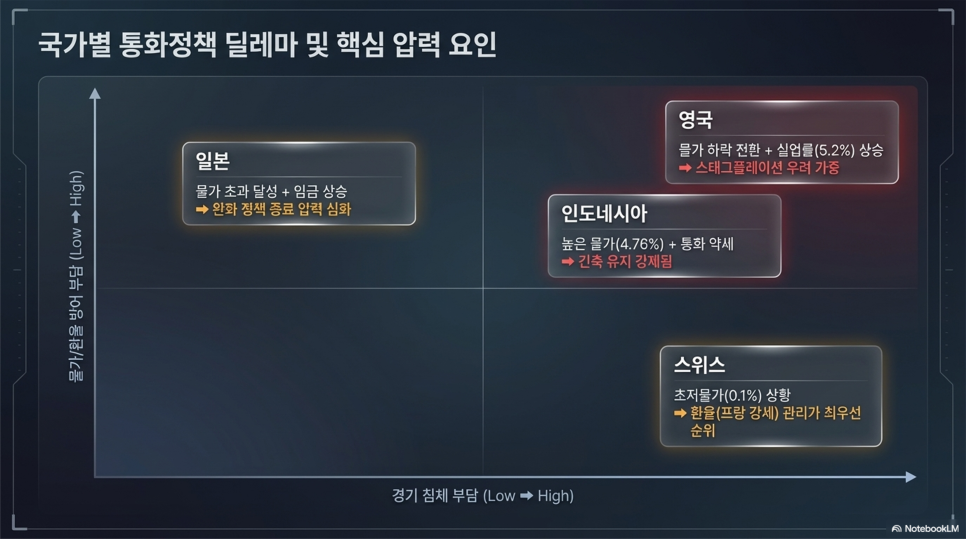

Japan

Japan's inflation rate has exceeded the target of 2% for nearly four years. In this situation, with wage increases occurring, it becomes challenging to continue the easing policy. Economic pressures are intensifying.

United Kingdom

The economic situation in the UK is intriguing. Currently, inflation is at 3.0%, and the unemployment rate has reached 5.2%.

These indicators point to a situation where prices are falling, but economic pressures are increasing.

Switzerland

The economic situation in Switzerland is quite different.

The current inflation rate is very low at 0.1%.

The rising demand for safe assets has increased the value of the Franc, making exchange rate management an important policy factor.

Indonesia

Indonesia's inflation rate has reached 4.76%. Currently, the local currency, the Rupiah, is weak, leaving almost no possibility for interest rate cuts.

Key Watching Points of this Meeting

The most critical question during this rate decision week is straightforward.

It is not “who is the decision-maker on interest rates,” but rather “how seriously do you take the oil shock from the Middle East?”

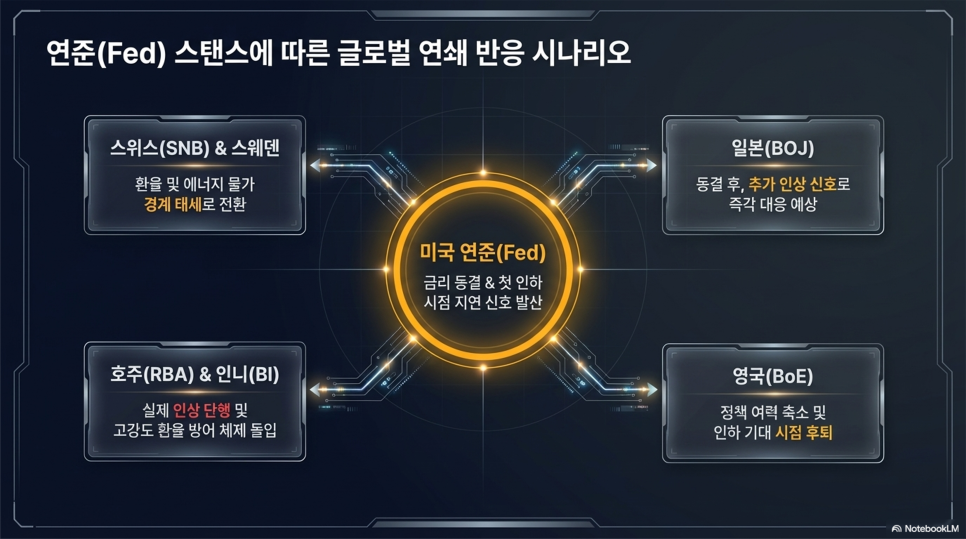

In particular, the remarks from the US Federal Reserve are very important.

Several possibilities can be considered here. Rates may stay the same, but the dot plot could shift in a hawkish direction.

In such a case, the market is likely to react as follows: expectations for a rate cut in June may weaken, and the first cut may be delayed until after September.

It is expected that various central banks will display similar movements. Japan is signaling additional rate hikes after freezing rates, while the UK is postponing expectations for rate cuts. Switzerland is running its policy centered around the exchange rate, and Sweden is cautious of rising energy prices. Australia is seriously considering the possibility of a rate hike. Indonesia appears to be focused on defending its currency.

As a result, it seems likely that next week will not be a week where central banks around the world cut rates simultaneously, but rather one that may realign in a hawkish direction.

Conclusion on Global Financial Market Outlook

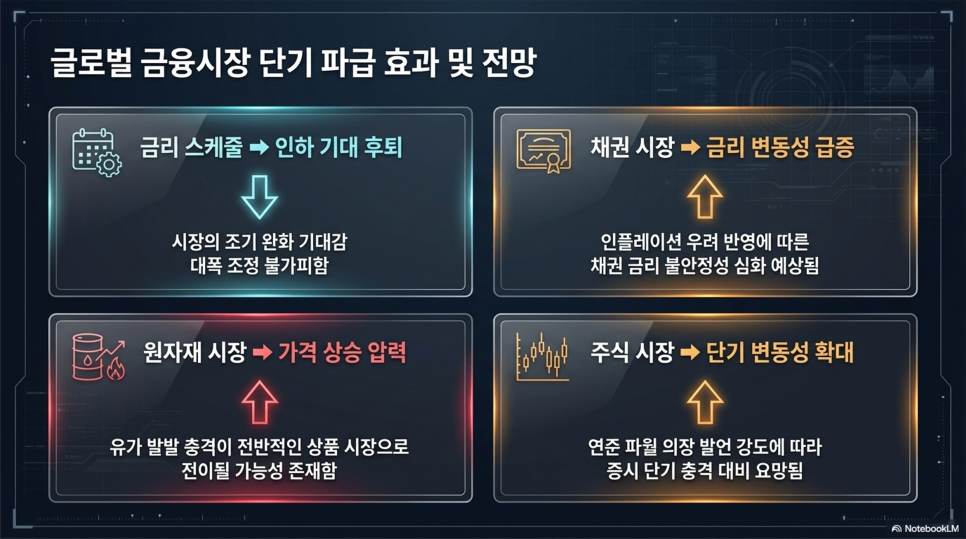

This Super Week of central banks in March focuses on three main factors. Firstly, oil prices are rising due to the war in the Middle East; secondly, the possibility of re-inflation is emerging; and lastly, expectations for interest rate cuts appear to be delayed.

When these three factors act simultaneously, the global financial market may experience shifts in a particular direction.

First, expectations for interest rate cuts may weaken. Second, volatility in the bond market may increase. Third, upward pressure on commodity prices is anticipated.

Furthermore, the stock market is also expected to see increased short-term volatility.

Therefore, this week, financial markets may react more sensitively to the FOMC dot plot, Chairman Powell's remarks, and the central banks' interpretations of inflation than to the interest rate decisions.

#RateDecisionSuperWeek, #FOMCmeeting, #FedRateOutlook, #GlobalCentralBanks, #InterestRatePolicy, #BOJRate, #BankOfEnglandRate, #SwissNationalBank, #ReserveBankOfAustralia, #IndonesiaRate, #GlobalRateOutlook, #GlobalInterestRates, #InterestRateHoldOutlook, #RateCutOutlook, #DotPlotOutlook, #PowellPressConference, #OilPriceIncrease, #MiddleEastWarImpact, #EnergyInflation, #ReInflation, #GlobalEconomicOutlook, #WorldEconomicAnalysis, #BondRateOutlook, #FinancialMarketOutlook, #CommodityMarket, #InternationalOilPriceOutlook, #MonetaryPolicyAnalysis, #MacroeconomicAnalysis, #EconomicOutlook, #InvestmentStrategy

Frequently Asked Questions (FAQ)

Q. What is the Rate Decision Super Week in March 2026?

It refers to the period from March 16 to 20, when major central banks hold simultaneous monetary policy meetings.

From March 16 to 20, 2026, multiple major central banks will hold simultaneous monetary policy meetings, marking a significant period. This period is commonly referred to as "Rate Decision Super Week", which greatly influences the global financial markets. Key announcements of interest rates and policy decisions by major central banks such as the US Federal Reserve (FOMC), Bank of Japan (BOJ), Bank of England (BoE), and Swiss National Bank (SNB) will be concentrated during this time.

Q. What is the most noteworthy aspect of this Super Week?

The key watching point is the quarterly outlook and dot plot announcement from the US FOMC.

The most crucial aspect to watch during this Super Week is the US Federal Open Market Committee (FOMC) announcing its quarterly economic outlook and dot plot. This offers insights beyond just simple interest rate hikes or holds, significantly affecting market expectations for future interest rate paths. Chairman Powell's press conference is also a vital event that may indicate future monetary policy directions.

Q. How is the interest rate outlook for the US Federal Reserve?

The key interest rate is expected to be maintained at around 3.50–3.75%.

The US Federal Reserve is expected to maintain its key interest rate at around 3.50–3.75%. However, the anticipated timing for rate cuts is likely to be delayed, with a higher possibility of occurring in June or after September than previously expected. The rise in oil prices due to the war in the Middle East is contributing to concerns over inflation resurgence, which is affecting the timing of potential rate cuts.

Q. What is the policy direction expected from the Bank of Japan (BOJ) during this Super Week?

The Bank of Japan is likely to maintain its policy rate at 0.75% but may signal the possibility of additional hikes.

The Bank of Japan is expected to maintain its policy rate at the current level of 0.75%. However, with inflation rates exceeding the targets and wage increases occurring, it is increasingly difficult to sustain the easing policy. Therefore, there is a possibility of signaling additional rate hikes following a freeze during this meeting, which may serve as an important signal for the financial markets.

Q. What is the impact of the Middle East war and rising oil prices on interest rate decisions?

Rising oil prices from the Middle East war are increasing concerns about re-inflation, delaying expectations for interest rate cuts.

The war in the Middle East has led to rising international oil prices, and the increase in energy prices is intensifying inflationary pressures. This heightened concern over "energy-induced re-inflation" is influencing central banks to opt for holding or raising rates rather than cutting them. Consequently, markets are now facing a retreat in expectations for rate cuts and increased volatility.