Table of Contents

Key Insights on Raicom Investment Outlook

The most important point in Raicom's investment outlook is not just the approach to simple optical communication-related stocks, but how to assess the quality of the actual transition to profitability and its sustainability. These factors are expected to have a significant impact on future investment decisions.

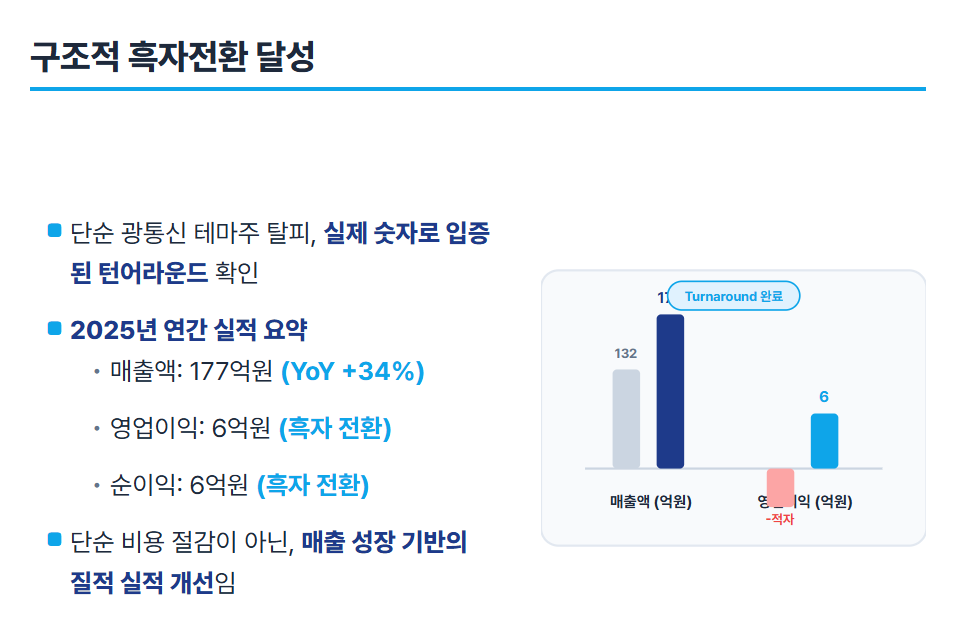

In 2025, the annual revenue reached KRW 17.7 billion, and both operating and net profits recorded at KRW 600 million, successfully achieving a transition to profitability. This can be interpreted as a signal of structural change. In particular, the fact that revenue increased by over 34% compared to the previous year holds significant meaning in that it shows recovery based on revenue growth rather than cost reduction.

For small to mid-cap tech stocks, temporary improvements and structural improvements can lead to completely different outcomes in market evaluations. This change is likely to act as a positive signal for investors.

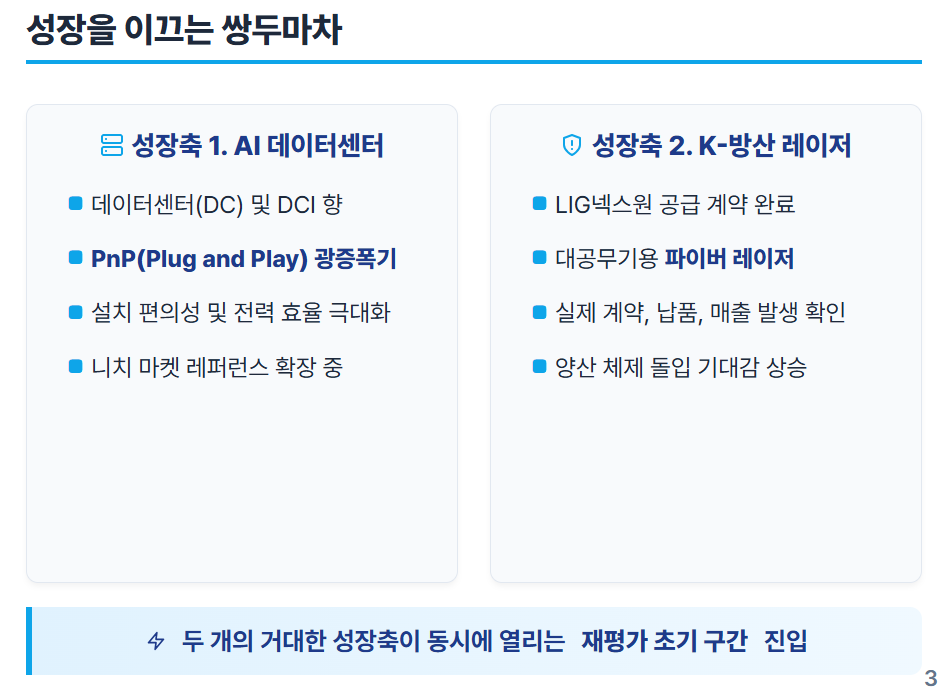

Raicom cited the increase in supply of PnP optical amplifiers for AI data centers and the commercialization of fiber laser defense sales as the reasons behind the performance improvement. The simultaneous operation of these two factors suggests a greater potential for growth.

AI Data Center Optical Amplifiers

Raicom is focusing on optical amplifier technology. However, more importantly from an investment perspective is the commercialization potential rather than technological innovation. The PnP (Plug and Play) optical amplifier is competitive due to its ease of installation and replacement in data centers and DCI (Data Center Interconnect) environments. This convenience greatly influences success in the market.

Due to the expansion of AI infrastructure, global data centers continue to be expanded. Along with this, optical communication equipment is gaining importance in terms of energy efficiency, space utilization, and operational convenience. Raicom provides form factor-based products to meet these practical needs, giving it an advantage.

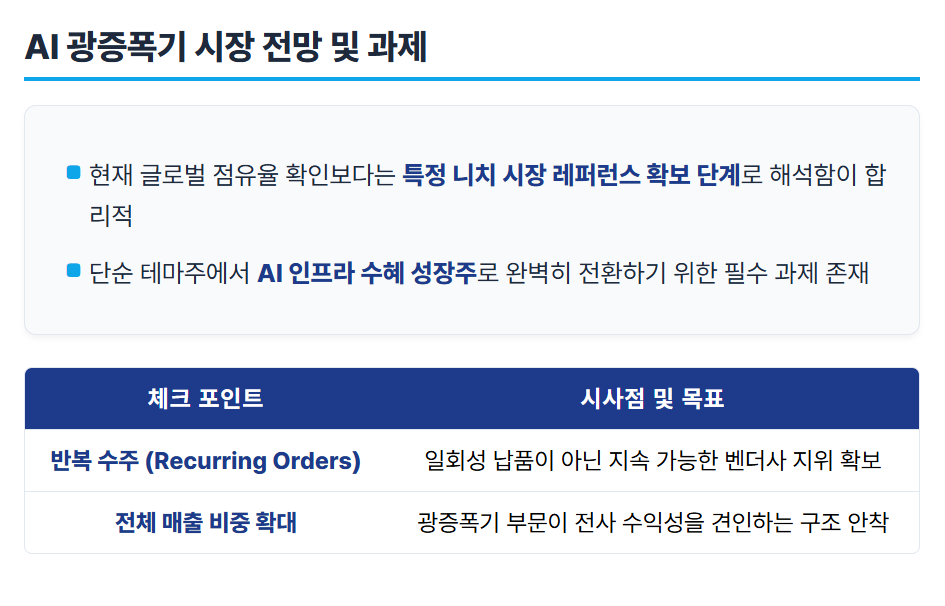

However, the current market share in the global market is not clearly revealed, and it is reasonable to understand it as being in the initial stage of increasing references in specific niche markets.

If in the coming quarters, repeated orders and an increase in sales proportion are confirmed, Raicom is likely to be re-evaluated as a growth stock benefiting from AI infrastructure rather than merely a thematic stock.

Expansion of Defense Laser Sales

The second growth driver receiving attention is defense lasers.

Raicom has achieved the commercialization of fiber lasers for anti-aircraft weapons through a KRW 5.3 billion supply contract for laser modules with LIG Nex1. This holds great significance as it has led to actual contracts, deliveries, and revenue recognition, not just simple expectations.

Due to the nature of defense projects, revenue recognition can show significant fluctuations each quarter. In this case, important factors are the subsequent orders and the possibility of expanding mass production. If defense lasers form a repetitive revenue structure, Raicom's revenue structure could greatly improve.

If the mass production of AI data center optical amplifiers and defense lasers occurs concurrently, it can secure both performance stability and growth potential. This could lead to a re-evaluation of valuation multiples.

Weekly Chart and Valuation Analysis

The current stock price is moving around KRW 2,900, and has shown a gradual upward trend after forming a low point based on weekly charts. The area around KRW 3,000 serves as a psychological resistance line, and breaking through the range of KRW 3,200 to KRW 3,400 is considered a key factor for mid-term trend reversal. Conversely, if it falls below KRW 2,500, the possibility of adjustments should also be kept in mind.

The financial state has moved past historical deficits and has entered the early stages of transitioning to profitability. It is more effective to approach the current situation based on PBR rather than PER.

The current PBR is reaching the mid-3 range, and when reflecting the expected BPS, a reasonable target PBR of 4 to 4.5 times leads to a primary target stock price of approximately KRW 3,500.

If the premium theme expands, there is a scenario where the PBR could reach 8 to 10 times, but this is only possible if several conditions are met.

Firstly, repeated orders in the AI data center need to be confirmed, and subsequent contracts for defense lasers are also necessary. Additionally, it is essential for quarterly results to maintain profitability and for the focus on small-cap stocks to be concentrated.

During an overheating phase, multiples could expand up to KRW 6,600 to KRW 8,300, but it is necessary to approach this separately from fundamental-based target prices.

Summary of Raicom Investment Outlook

The most critical factor in Raicom's investment outlook is the sustainability of the transition to profitability. Recent results are interpreted not just as a simple event but as a result of the simultaneous expansion of supply of PnP optical amplifiers for AI data centers and increased sales from defense lasers. This can be seen as a signal of possible structural change.

However, it is still early to declare it a "confirmed high-growth stock." It is in the early stage of a performance re-evaluation. Therefore, it is essential to closely monitor quarterly sales composition, operating profit margins, and the status of repeated orders moving forward.

In summary,

the target stock price based on fundamental fundamentals is around KRW 3,500. If the theme expands, the overheating target price could range between KRW 6,600 and KRW 8,300. The key elements in this process will be the sustainability of sales in AI data centers and subsequent orders in the field of defense lasers.

Raicom has reached a point where its value is validated by actual numbers, not just discussions. Therefore, future stock prices will heavily depend on the sustainability of performance and the expansion of multiples.

#Raicom, #RaicomInvestmentOutlook, #AIDataCenter, #DCI, #OpticalAmplifier, #PnPOpticalAmplifier, #DefenseLaser, #FiberLaser, #LIGNex1, #OpticalCommunicationStocks, #CommunicationEquipmentStocks, #SmallCapAnalysis, #TransitionToProfitability, #TurnaroundStocks, #PBRAnalysis, #TargetStockPrice, #WeeklyChart, #TechnicalAnalysis, #AIInfrastructure, #DataCenterBenefactorStocks, #AerospaceRelatedStocks, #SatelliteCommunication, #DefenseRelatedStocks, #GrowthStockAnalysis, #SmallAndMidCapStocks, #ThemeStockAnalysis, #StockInvestmentStrategy, #CorporateValuation, #FinancialAnalysis, #2026StockOutlook

Frequently Asked Questions (FAQ)

Q. What does the improvement in Raicom's performance in 2025 mean?

Raicom achieved structural transition to profitability in 2025 with a revenue of KRW 17.7 billion and an operating profit of KRW 600 million.

In 2025, Raicom's revenue increased by over 34% compared to the previous year, reaching KRW 17.7 billion, while both operating and net profits were KRW 600 million, successfully transitioning to profitability. This achievement is seen as a positive signal for investors as it indicates structural improvement based on revenue growth rather than mere cost reduction. Temporary improvements and structural improvements in small to mid-cap tech stocks can make a significant difference in market evaluations, and Raicom's recent performance suggests sustainable growth potential.

Q. What are the main drivers of Raicom's growth?

The expansion of PnP optical amplifiers for AI data centers and defense laser sales are the main growth drivers for Raicom.

Raicom identifies the increase in supply of PnP optical amplifiers for AI data centers and the resulting revenue from the commercialization of fiber laser defense as its main growth drivers. In particular, PnP optical amplifiers are competitive in data center environments due to their ease of installation and replacement, and a supply contract worth KRW 5.3 billion with LIG Nex1 has secured a stable revenue base in the defense sector. The commercialization and revenue expansion in these two business divisions are contributing to performance improvement and revenue structure stability.

Q. What is the current situation of Raicom's stock price?

Raicom's stock price is showing a gradual upward trend after forming a low point around KRW 2,900.

Currently, Raicom's stock price is around KRW 2,900, and after forming a low point on the weekly chart, it is gradually trending upward. The area around KRW 3,000 serves as a psychological resistance line, and breaking through the range of KRW 3,200 to KRW 3,400 is important for a mid-term trend reversal. Conversely, if it falls below KRW 2,500, adjustments may also be possible, so it is necessary to closely monitor stock price movements when investing.

Q. What are the key evaluation indicators in Raicom's investment outlook?

The sustainability of the transition to profitability and the repeated orders in AI data centers and defense business are key evaluation factors.

The most important aspect of Raicom's investment is to determine whether the transition to profitability is a sustainable structural change rather than a temporary event. The simultaneous increase in sales of PnP optical amplifiers for AI data centers and defense lasers can be seen as a positive signal. Moving forward, it is essential to comprehensively verify quarterly sales composition, operating profit margins, and the status of repeated orders, as these will be critical elements leading investors to re-evaluate.

Q. What are the target stock price and multiple outlook for Raicom?

The basic target stock price is about KRW 3,500, and if the theme expands, there is a possibility of rising between KRW 6,600 and KRW 8,300.

According to financial analysis, Raicom's reasonable target stock price is about KRW 3,500 when applying a PBR of 4 to 4.5 times. If repeated orders in the AI data center field and subsequent contracts for defense lasers are confirmed, it could be evaluated as a premium theme in the market, potentially expanding PBR to 8 to 10 times, leading to an overheating target price between KRW 6,600 and KRW 8,300. However, this multiple expansion requires stable performance growth and concentration on market supply and demand, necessitating an approach that distinguishes fundamentals in investing.