Table of Contents

- Monthly pension of 10 million won, it becomes clear when broken down into numbers

- Key points for calculating monthly compound interest returns

- Calculating 11 million won monthly from a pension fund of 3 billion won

- How to manage pension savings funds using ETFs

- Yearly year-end target balance table

- Conclusion: Achieving 10 million won monthly is a matter of strategy

- Frequently Asked Questions (FAQ)

Monthly pension of 10 million won, it becomes clear when broken down into numbers

"The goal of receiving a monthly pension of 10 million won may seem vague, but by breaking down the necessary returns and pension resources, a clearer plan can be formed.

This article will take the author in their late 30s as a basis, starting with 35 million won and planning to contribute 6 million won each year at the beginning of the year for 15 years. This will aim for about 3 billion won in 15 years, and I will mathematically calculate and summarize it.

Furthermore, recently various ETFs (exchange-traded funds) have emerged, providing more opportunities for active investment within pension savings funds. Considering this, it is important to further develop the strategy."

Previously, I dealt with fund investments for collateral loans through pension accounts. As market volatility has increased recently, funds are being reorganized, and all capital is being invested in ETFs.

I regularly check the trading history of the pension savings account, and plan to share the results by checking the target return rate and balance achievement at the end of each year.

Recommended Articles

Key points for calculating monthly compound interest returns

The core concept can be explained simply. Assuming that the operational profits increase at the same rate monthly in compound interest form, and that additional contributions of 6 million won are made at 12-month, 24-month, ... , 180-month intervals, the assets after 180 months (15 years) will show the result of adding the compound growth of the initial capital and the compound growth of the remaining duration of the contributions.

Calculating this equation to fit 3 billion won, the required monthly return rate turns out to be around 2%. In practice, it is important to clearly distinguish between two types of returns.

First, the nominal annual return (APR) is simply derived by multiplying the monthly return by 12. Second, the effective annual return (EAR) is calculated reflecting the monthly compound effect as ((1+r)^{12}-1).

Ultimately, when using the term “monthly compound interest”, it means that the benchmark for long-term goals also shifts from nominal to effective. This understanding is essential in formulating an investment strategy.

Consistently achieving a 2% monthly compound interest over 15 years is a very challenging goal when considered against the volatility and downturns of stocks and ETFs. Therefore, the target return rate should be viewed not just as a simple hope, but also in terms of risk budgeting, considering whether one can withstand volatility and drawdowns.

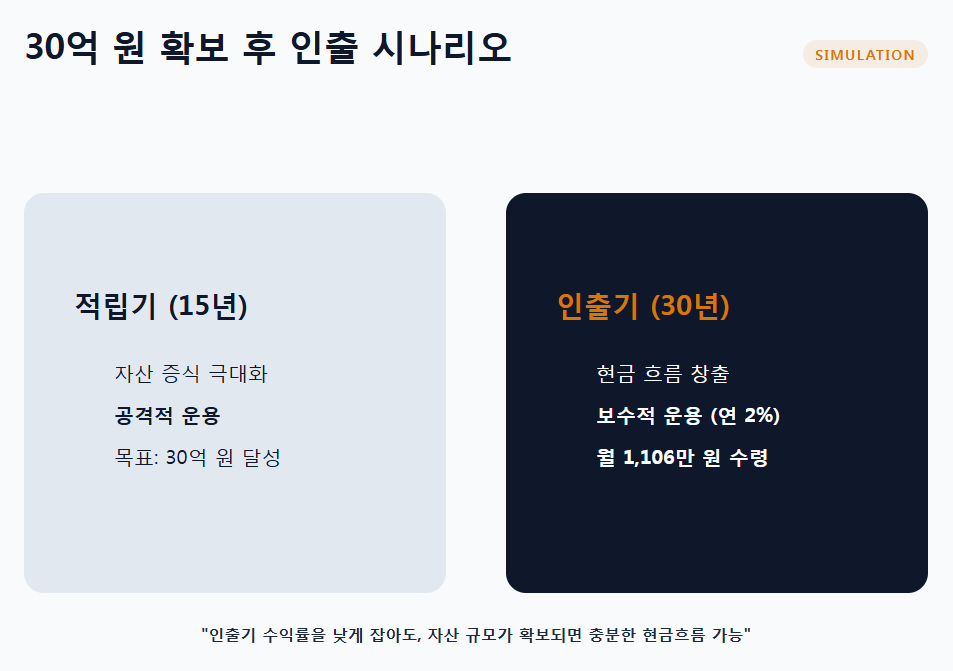

Calculating 11 million won monthly from a pension fund of 3 billion won

After accumulating 3 billion won as a pension, consider a defined pension that receives a fixed amount monthly for 30 years at an annual rate of 2%.

When converting the 2% annual rate into monthly compound interest, the monthly interest rate would be around (i=(1+0.02)^{1/12}-1). Using the present value of a defined pension to calculate the monthly payment amount, it results in approximately 11.06 million won per month (based on end-of-month payments). If calculated for early payment (beginning of the month), the payment amount would slightly decrease.

In conclusion, aggressive compound management is needed during the accumulation phase, but even assuming conservative operations (annual 2%) during the withdrawal phase, a structure is established that permits generating a return of about 11 million won monthly.

The key point here is that accumulation and withdrawal phases have different characteristics, and aggressive returns and conservative returns should not be compared on the same basis. This needs to be clearly understood.

How to manage pension savings funds using ETFs

When aiming to operate ETFs in a "project-style" using pension savings funds, the method is simple, but strict adherence to rules is crucial.

First, apply the core-satellite strategy. Select a broad market index ETF for the core part to ensure stability and seek excess returns through growth, thematic, quality, and dividend strategies in the satellite part.

Second, set rebalancing rules in advance. Choose one frequency from quarterly, biannual, or annual, and clearly establish criteria for adjustments when deviating from the target weight by ±○%.

Recently, various active ETFs have been released, allowing for a more proactive portfolio management than index ETFs in specific sectors (e.g., AI, space, robotics, secondary batteries, divisive growth, etc.). However, when selecting active ETFs, it is essential to consider the competency of fund managers, fees, and tracking errors.

Finally, if aiming for monthly compound interest, preventing deviations during drawdowns is even more important than stock selection. Ultimately, the success depends on sustainability rather than just "returns".

Yearly year-end target balance table

Assuming a starting amount of 35 million won, with an annual contribution of 6 million won over 15 years, a table has been compiled summarizing the year-end target balances. This is based on detailed reverse calculations according to monthly compound interest standards.

| Year | Year Number | Year-End Target Balance (Won) | Year-End Target Balance (Billion Won) | Simple Return Compared to Previous Year |

| 2026 | 1 | 53,177,293 | 0.53 | 51.94% |

| 2027 | 2 | 76,753,372 | 0.77 | 44.33% |

| 2028 | 3 | 107,331,715 | 1.07 | 39.84% |

| 2029 | 4 | 146,992,044 | 1.47 | 36.95% |

| 2030 | 5 | 198,431,775 | 1.98 | 34.99% |

| 2031 | 6 | 265,149,473 | 2.65 | 33.62% |

| 2032 | 7 | 351,682,805 | 3.52 | 32.64% |

| 2033 | 8 | 463,917,154 | 4.64 | 31.91% |

| 2034 | 9 | 609,485,907 | 6.09 | 31.38% |

| 2035 | 10 | 798,289,621 | 7.98 | 30.98% |

| 2036 | 11 | 1,043,169,386 | 10.43 | 30.68% |

| 2037 | 12 | 1,360,780,193 | 13.61 | 30.45% |

| 2038 | 13 | 1,772,723,678 | 17.73 | 30.27% |

| 2039 | 14 | 2,307,017,324 | 23.07 | 30.14% |

| 2040 | 15 | 3,000,000,000 | 30.00 | 30.04% |

Conclusion: Achieving 10 million won monthly is a matter of strategy

The project aiming for a monthly pension of 10 million won should be approached quantitatively without being swayed by emotions.

If aiming for 3 billion won over 15 years, this requires a very high yield based on monthly compound interest. The likelihood of success depends more on rebalancing rules, responses to market downturns, and the sustainability of regular contributions than on which ETFs to choose.

However, after defining a goal of 3 billion won, even assuming conservative operations with an annual yield of 2%, it is mathematically possible to receive about 11 million won monthly in a defined pension over 30 years.

Ultimately, the key is to actively manage ETFs within pension savings funds by setting rules first and considering emotions later. This can be considered a realistic method for pursuing long-term compounding.

#monthly pension 10 million won, #pension savings fund, #pension savings ETF, #ETF investment, #monthly compound interest, #compound investment, #pension resources, #retirement preparation, #defined pension, #pension calculation, #annual return rate, #effective yield, #nominal return, #asset allocation, #rebalancing, #core-satellite, #active ETF, #long-term investment, #retirement pension, #IRP, #ISA, #tax deduction, #pension portfolio, #index ETF, #thematic ETF, #dividend ETF, #growth stock ETF, #target asset, #wealth management, #investment strategy

Frequently Asked Questions (FAQ)

Q. What are the necessary pension resources and return rates for a monthly pension of 10 million won?

If you save for 15 years to accumulate around 3 billion won, you can achieve a monthly pension of 10 million won, requiring a monthly compound interest return rate of about 2%.

To aim for a monthly pension of 10 million won, starting with 35 million won at the age of late 30s and contributing 6 million won each year for 15 years can create about 3 billion won in pension resources. For this, a monthly compound interest return rate in the 2% range is necessary. This return rate should be recognized as an effective yield reflecting the compound effect, not as a nominal annual return, and it serves as the core criterion for long-term compound investments.

Q. What is the difference between nominal annual return and effective annual return when calculating monthly compound interest returns?

Nominal annual return is the figure obtained by multiplying the monthly return by 12, and the effective annual return is the actual annual return reflecting the compound effect.

Nominal annual return (APR) is simply calculated by multiplying the monthly return by 12, whereas effective annual return (EAR) is derived from the monthly return calculated on a compound basis as ((1+r)^12-1). The effective return accurately indicates the actual return when investing long-term because it reflects the compound effect. Thus, it is essential to establish an investment plan based on the effective annual return when setting a monthly compound interest target.

Q. What are effective strategies for managing ETFs within pension savings funds?

Applying a core-satellite strategy, establishing strict rebalancing rules, and considering the use of active ETFs are important.

ETF investments are recommended to adopt a core-satellite strategy. The core part should be focused on broad index ETFs for stability, while the satellite component can utilize various ETFs for growth, themes, quality, and dividends to pursue excess returns. Rebalancing criteria should be clearly defined in advance, and portfolia weights should be adjusted regularly. Additionally, active ETFs in sectors like AI, space, or dividend growth can be utilized, ensuring that the manager's competencies and costs are also considered, with an emphasis placed on sustainability over mere yield for successful management.

Q. What is the difference in management strategies between the accumulation phase and the withdrawal phase of pensions?

In accumulation, adopt an aggressive compound return strategy; in withdrawal, a conservative annual 2% operation should be assumed.

During the pension accumulation phase, a monthly aggressive compound return of about 2% is needed to achieve the target, while in the withdrawal phase, it is assumed that a conservative annual return of 2% is obtained. Growth-focused investments are crucial during the accumulation phase, and ensuring stable income is essential during the withdrawal phase, so the return rates and strategies of both periods should not be compared on the same basis. By efficiently distinguishing these phases, it is possible to provide a stable monthly pension of about 11 million won over a 30-year period.

Q. What is most important in achieving the goal of a monthly pension of 10 million won?

Setting rebalancing rules, reacting to drawdowns, and maintaining consistent contributions are key, rather than ETF selection.

The plan for a monthly pension of 10 million won should prioritize adhering to investment rules strictly, rather than simply selecting ETFs. Regular contributions should be maintained without being swayed by emotions, while strategies should be prepared for market volatility and downturns. Clearly set rebalancing criteria and a long-term perspective that prevents exiting during drawdown periods will determine success. Consistent management and planning are more reliable and realistic methods to build a pension than simply aiming for high rates of return.