Table of Contents

The Era of 100 Million Won Deposit Protection Limit

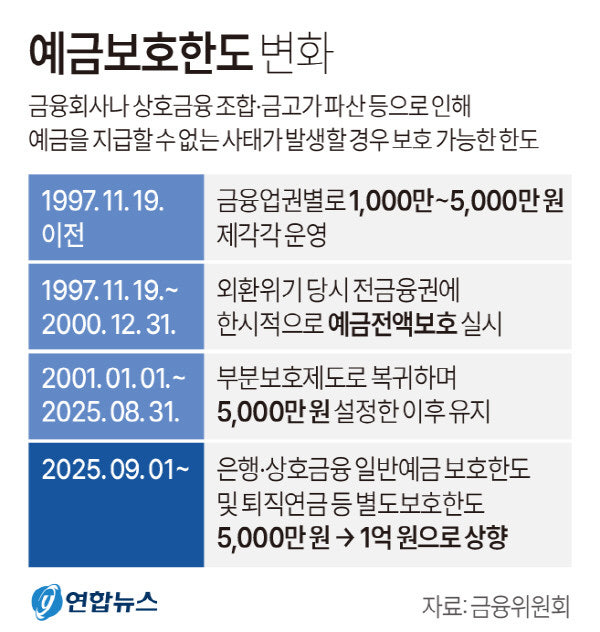

Starting from September 1, 2025, the deposit protection limit will increase from the current 50 million won to 100 million won. This adjustment, made for the first time in 24 years since 2001, is a significant change aimed at better safeguarding the assets of financial consumers.

This change will be uniformly implemented across all financial institutions where deposit protection applies, including banks, savings banks, credit unions, agricultural cooperatives, Saemaul Geumgo, and post offices. Notably, it will also apply retroactively to existing products. This is considered a crucial change that will significantly influence the asset management strategy of the public.

Implementation Date and Decision Process

The increase in the deposit protection limit was finalized at the cabinet meeting on July 22, 2025. This measure is set to take effect on September 1, 2025.

The Korea Deposit Insurance Corporation and mutual financial institutions have been checking and preparing their systems for several months.

This adjustment is considered an unavoidable measure reflecting rising prices and changes in the financial environment.

Major Changes

With the recent amendment to the Deposit Protection Act, the total of the principal and interest deposited in the same financial institution can now be protected up to 100 million won.

For example, if you deposit 150 million won at Bank A, only 100 million won will be protected, and the remaining 50 million won will not be covered. However, if you deposit 80 million won at Bank A and 80 million won at Bank B, the protection limit of 100 million won applies at each bank, ensuring a total of 160 million won is safely protected.

In conclusion, the principle of protection applied per financial institution still holds, which continues to make the strategy of diversified deposits effective.

Retrospective Application

One of the notable aspects of this amendment is that it will be applied retroactively. Savings and insurance products subscribed before September 1 will also be subject to the new protection limit.

As a result, products that were previously covered up to 50 million won will automatically be protected up to 100 million won after the implementation.

Protected and Non-Protected Products

Protected Products

Examples of financial products that are typically covered include savings accounts, term deposits, and insurance surrender values. Additionally, retirement pensions (IRP, DC, etc.) and annuity savings are considered important assets. Foreign currency deposits are managed in converted won, and post office deposits have the characteristic of being fully protected. These various financial products are essential for stable asset management.

Non-Protected Products

There are performance-based investment products such as stocks, funds, ELS, and DLS. CMA and RP accounts offered by securities firms are also among the investment options. However, products with uncertain principal guarantees, such as variable insurance or subordinated bonds, are not protected.

In conclusion, only deposit-type products with guaranteed principal can be protected, and investment-type products are not included in the list of protected items.

Deposit Strategies and Precautions

This change in the system is expected to lead to changes in the asset management methods of depositors.

First, the strategy of diversified deposits remains effective. By using various financial institutions such as banks, savings banks, and credit unions, up to 100 million won will be protected at each institution, allowing for safer management of larger amounts through the use of multiple institutions.

Second, attention is required regarding whether interest is included. Since the limit of 100 million won is set by adding both principal and interest, it is essential to verify if the total exceeds this limit.

Third, various entities within the financial group are also subject to separate protection. For instance, KB Kookmin Bank and KB Savings Bank can both be protected up to 100 million won each.

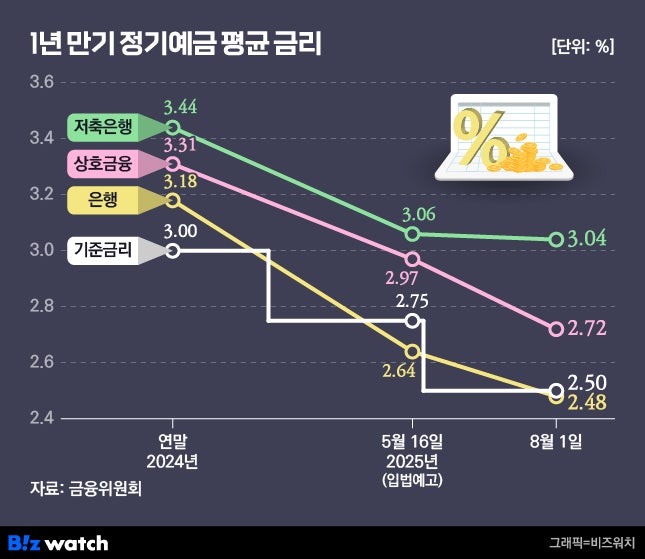

Furthermore, a shift of funds towards savings banks and mutual finance is anticipated. Though funds may concentrate on high-interest savings and deposit products, it is crucial to assess the soundness of these institutions.

Lastly, there is a possibility of an increase in the deposit insurance premium rate in the future. From 2028, the burden on financial institutions is expected to rise, and it will be necessary to consider potential fluctuations in deposit interest rates or fees in the long term.

Impact of the Implementation

Raising the deposit protection limit is not just a numerical change, but plays a pivotal role in enhancing overall trust and stability in the financial market.

As a result, not only high-value depositors but also ordinary depositors can feel a sense of psychological relief, knowing that even in the event of a financial institution's bankruptcy, their funds up to 100 million won will be safely protected.

However, since not all financial products are protected, financial consumers need to carefully examine the characteristics and risks of each product.

Conclusion

The adjustment to the deposit protection limit, which will be implemented on September 1, 2025, is a significant change that provides considerable stability for financial consumers.

This benefit will also apply to existing financial products, allowing consumers to manage their assets with peace of mind. Implementing a diversified deposit strategy is also a good method for more systematic asset management.

However, investment-type products are excluded from protection, so it is crucial to thoroughly review the stability of financial institutions and the structure of products. This policy change is expected to have a substantial impact on the public's asset management approach.

#DepositProtectionAct, #DepositProtectionLimit100Million, #DepositProtectionImplementationDate, #BankDeposits, #SavingsInterestRates, #DepositsSavings, #SavingsBankDeposits, #SaemaulGeumgoDeposits, #CreditUnionDeposits, #AgriculturalCooperativeDeposits, #FisheriesCooperativeDeposits, #ForestryCooperativeDeposits, #PostOfficeDeposits, #DepositProtection, #FinancialConsumers, #RetrospectiveApplicationOfDepositProtection, #DepositProtectionTarget, #DepositProtectionProducts, #NonDepositProtection, #DepositProtectionInterest, #DiversifiedDeposits, #HighInterestSavings, #FinancialStability, #KoreaDepositInsuranceCorporation, #AmendmentToDepositProtectionAct, #DepositProtectionByFinancialInstitution, #FirstFinancialSectorDeposits, #SecondFinancialSectorDeposits, #DepositInvestmentStrategies, #DepositStrategies

Frequently Asked Questions (FAQ)

Q. When will the deposit protection limit be raised to 100 million won?

The deposit protection limit will increase to 100 million won starting from September 1, 2025.

Starting from September 1, 2025, the existing deposit protection limit of 50 million won will be raised to 100 million won. This adjustment is an important measure to strengthen the protection of financial consumers' assets, and it will be uniformly implemented across all financial institutions where deposit protection applies.

Q. Which financial institutions will the increase in the deposit protection limit apply to?

It will be uniformly applied to all financial institutions providing deposit protection, including banks, savings banks, credit unions, agricultural cooperatives, Saemaul Geumgo, and post offices.

This increase in the limit will apply to all financial institutions where deposit protection is available, including banks, savings banks, credit unions, agricultural cooperatives, Saemaul Geumgo, and post offices. Since each financial institution provides protection up to 100 million won, asset management can be made safer through diversified deposits.

Q. Will the increase in the deposit protection limit be applied retroactively to existing products?

Yes, savings and insurance products subscribed before September 1, 2025, will also be retroactively covered up to 100 million won.

This amendment to the Deposit Protection Act includes retrospective application, so savings and insurance products subscribed before September 1 will benefit from the new protection limit of 100 million won. Thus, products that were previously guaranteed only up to 50 million won will automatically have their coverage expanded, allowing financial consumers to feel secure.

Q. What are protected financial products and non-protected products?

Principal-guaranteed deposits and insurance surrender values are protected, while investment products like stocks and funds are non-protected.

Protected products include deposits, term deposits, insurance surrender values, retirement pensions, and annuity savings, which offer principal guarantees. In contrast, investment products such as stocks, funds, ELS, DLS, CMA, and RP accounts, as well as variable insurance and subordinated bonds that lack principal guarantees, are excluded from deposit protection. Therefore, it’s essential to be cautious as investment products do not receive protection.

Q. Is the diversified deposit strategy still valid within the 100 million won protection limit?

Yes, since 100 million won is protected per financial institution, diversification across several institutions provides cumulative protection.

Deposit protection applies per financial institution, so for instance, if deposited in both Bank A and Bank B, both will have individual protection up to 100 million won. Consequently, high-net-worth individuals can protect larger amounts by diversifying deposits across various institutions. Thus, the strategy of diversified deposits remains effective even after this implementation change.

Q. What should financial consumers be cautious of regarding the increase in the deposit protection limit?

Pay attention to whether interest is included, separate legal entity protection in financial groups, and ensuring the soundness of financial institutions.

The deposit protection limit of 100 million won is based on the combined total of principal and interest. Therefore, it is essential to confirm that the total amount including interest does not exceed the limit. Additionally, separate entities within a financial group (e.g., KB Kookmin Bank and KB Savings Bank) are protected up to 100 million won each, so this can be utilized. Furthermore, when shifting funds to high-interest products at savings banks or mutual finance institutions, it is crucial to check the soundness of the institutions.

Q. What impact will the increase in the deposit protection limit have on the financial market?

It will enhance financial stability and trust, providing psychological comfort to depositors and strengthening the soundness of financial institutions.

Raising the deposit protection limit serves not only to increase the protected amount but also plays a role in improving trust in the financial market and enhancing stability. Both high-value depositors and ordinary depositors will feel psychologically secure, knowing that they can securely protect up to 100 million won even in the event of a financial institution's bankruptcy. However, not all products are protected, so financial consumers should carefully review product traits.