Table of Contents

- 2025: A Major Shift in Tax Policy Transforming Our Lives

- Strengthening Tax Support for Leap Toward an Economic Powerhouse

- Warm Tax Policies for Livelihood Stabilization: Expansion of Support for Ordinary and Middle-Class Citizens

- Normalization of Tax Burden to Expand Revenue Base

- The 2025 Tax Reform Plan: Expectations and Challenges

- Frequently Asked Questions (FAQ)

2025: A Major Shift in Tax Policy Transforming Our Lives

The Ministry of Economy and Finance has announced the 2025 tax reform plan based on the vision of a 'fair and efficient tax system for true growth.'

This reform plan has been developed considering the complex economic environment due to population structure changes, stagnation of productivity leading to declining potential growth rates, and increased welfare expenditures from aging.

The government has outlined three main policy directions to move toward becoming an economic powerhouse, promote the stabilization of livelihoods, and strengthen the weakened revenue base.

This tax reform plan is expected to have a broad impact, from the investment environment for companies to the households of individuals, highlighting the need for a more in-depth analysis of its core contents.

Strengthening Tax Support for Leap Toward an Economic Powerhouse

The government plans to significantly expand support for future strategic industries for sustainable growth and the future of the economy. This will help secure new revenue sources and promote economic development.

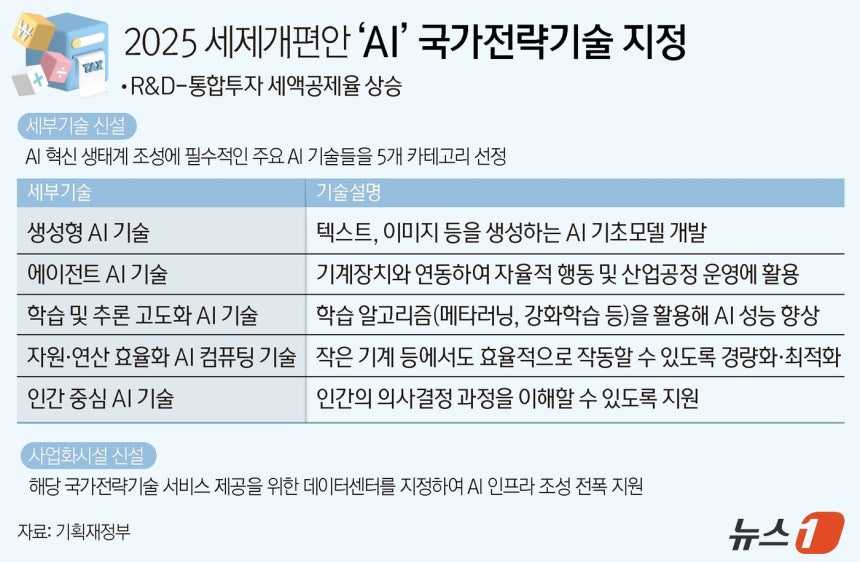

Focused Support for Future Strategic Industries: AI, Semiconductors, and K-Content

In the field of AI, 'generative AI technology,' which creates text and images, and 'agent AI technology,' which autonomously performs tasks in collaboration with machines, will be designated as national strategic technologies.

Additionally, the tax credit for facility investments in data centers will be expanded. Companies will be able to receive up to a 50% research and development (R&D) tax credit and a 30% investment tax credit, depending on their size.

Furthermore, to facilitate the return of AI experts and outstanding talents from abroad, the application period for a system that provides a 50% income tax reduction for ten years will be extended by three years. These measures are seen as efforts to further develop Korea's AI industry.

Recently, various support measures have been established to enhance the competitiveness of the K-content industry. In particular, a tax credit for production costs such as labor costs and royalties necessary for webtoon content creation will be newly introduced. Small businesses will receive a 15% credit, while large and medium-sized companies will receive a 10% credit, significantly promoting creative activities in the domestic webtoon industry.

Additionally, the tax credit for video content production costs will be improved. The base credit rate for large and medium-sized companies will increase from 5% to 10%, and the application period will be extended by three years, further enhancing the foundation for the sustainable growth of K-content. This support is expected to play a crucial role in boosting the global competitiveness of K-content.

Revitalization of Capital Markets and Promotion of Corporate Investment

To revitalize the capital market, a tax reform for high-dividend companies is necessary. A plan must be considered to apply a separate tax rate of a maximum of 35% instead of the comprehensive income tax (up to 45%). Additionally, dividend income should be included in the return targets for the investment and cooperative promotion tax system, and the ratio of income that companies should return should be increased.

These measures will help ensure that corporate profits are widely shared with shareholders and society. As a result, it is expected to positively impact the economy by simultaneously encouraging corporate investment and dividends.

Warm Tax Policies for Livelihood Stabilization: Expansion of Support for Ordinary and Middle-Class Citizens

This tax reform plan includes various support measures aimed at effectively reducing the tax burden on ordinary and middle-class citizens and responding to the low birth rate issue. Such changes are expected to contribute to increasing economic stability.

Support for Overcoming Low Birth Rates: Significant Strengthening of Benefits for Multi-Child Households

The most notable change is the increase in the ceiling for credit card income deductions for multi-child households. Previously, the same deduction limit applied regardless of the number of children, but now, for employees with a total salary of 70 million won or less, the basic deduction limit will increase by 500,000 won per child, up to a maximum of 1 million won.

Additionally, there will be changes to the tax-exempt ceiling for childcare allowances for children under six years old. The previous monthly limit of 200,000 won will expand to 200,000 won per child monthly, which is expected to significantly reduce the childcare burden on multi-child households. These changes are expected to have a positive impact on the economic stability of households.

Creating Strong Support Through Relief of Education and Housing Burdens

Policies to alleviate the burden of education and housing costs have been further strengthened. The tuition fees for extracurricular programs for elementary school students in grades 1 and 2 will now be added to the tax credit for education expenses, allowing for a 15% tax credit within an annual limit of 3 million won.

Furthermore, to support housing stability, the criteria for rental tax credit-eligible housing for households with three or more children will be expanded to 100 square meters regardless of the region, broadening the housing choices for multi-child households. These changes are expected to help reduce the economic burdens on households.

Tailored Tax System for Middle-Aged and Small Business Owners

To ensure the stable retirement of the middle-aged, the withholding tax rate for private pensions paid in a lifetime will be reduced from 4% to 3%. Additionally, a new segment will be created for the tax reduction rate to be expanded to 50% when receiving retirement income for 20 years or more. These changes are expected to reduce the tax burden on pension income.

To support small businesses, the additional limit on company expenses using regional love gift certificates has been doubled from the previous 10% to 20%. This designed policy helps provide tangible benefits to local businesses and small businesses.

Normalization of Tax Burden to Expand Revenue Base

The government has decided to implement 'normalization' measures to adjust some tax rates and standards back to previous levels in order to restore fiscal soundness and support active fiscal management.

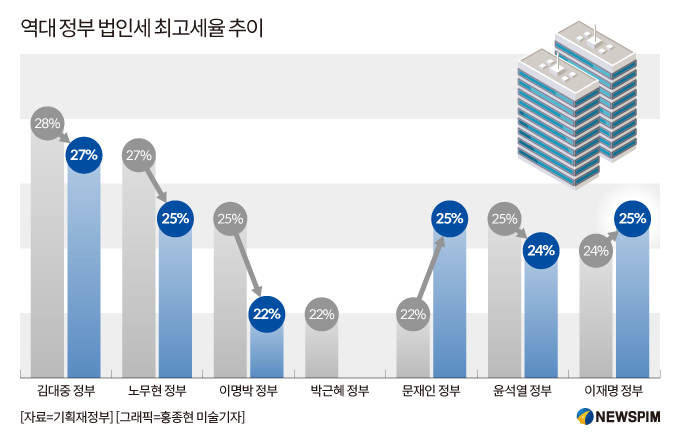

Restoration of Corporate Tax Rates and Financial Investment Taxation Standards

The most noticeable change is the restoration of the corporate tax rate. The corporate tax rate reduced in 2023 will revert to the 2022 level, applying rates ranging from 10% to 25% with a 1% point increase based on the tax standard segment.

There are also several changes in the capital market sector. The securities transaction tax rate and the threshold for capital gains tax on large shareholders will return to previous levels. The securities transaction tax rate on the KOSPI, which was expected to decrease to 0% starting in 2025, will be adjusted to 0.05%, while the KOSDAQ will see an increase from 0.15% to 0.20%.

Additionally, the thresholds for imposing capital gains tax on large shareholders in listed stocks will also be tightened. The holding amount per stock will be adjusted from 5 billion won to 1 billion won or more, broadening the tax base. These changes are expected to have significant impacts on investors and corporations.

Rationalization of the Tax System and Compliance with International Standards

If the income in the financial and insurance sectors exceeds 1 trillion won, the education tax rate will be raised from the existing 0.5% to 1.0% to normalize the tax burden of certain industries. Additionally, a domestic minimum tax (DMTT) will be introduced for multinational corporations receiving low taxation to facilitate the introduction of the global minimum tax system. These measures are aimed at preventing tax evasion and strengthening tax jurisdiction, as a strategy to stabilize national tax revenue, which has shown a decreasing trend over the past two years, and to activate the role of fiscal management.

The 2025 Tax Reform Plan: Expectations and Challenges

The 2025 tax reform plan is the result of the government's deep contemplation, aiming to achieve the goals of securing future growth engines, stabilizing livelihoods, and enhancing fiscal soundness simultaneously.

Through this reform, the government anticipates securing approximately 8.1672 trillion won in additional tax revenue over the next five years, with corporate tax increases being expected to account for the largest share, approximately 4.5815 trillion won.

The expansion of support for future technology sectors and K-contents is expected to contribute to improving the economic structure and creating new growth engines. Moreover, tailored support for multi-child households, ordinary citizens, and the middle class will effectively reduce household burdens.

According to the analysis of the tax burden, the tax burden on ordinary citizens and the middle class is expected to decrease by 102.4 billion won, while the tax burden on large corporations is expected to increase by 4.1676 trillion won. Such changes will further highlight the goals of the tax reform and contribute to increasing social equity.

The restoration of corporate tax rates and the capital gains tax thresholds could pose a significant burden on corporate investment sentiment and the capital market, warranting careful monitoring of future economic conditions.

This tax reform plan is scheduled for legislative notice and cabinet meeting in August, with a plan to submit it to the regular National Assembly in early September. Continuous attention is needed regarding the significant changes that will impact the national economy and households.

#2025TaxReformPlan, #Tax, #CorporateTax, #SecuritiesTransactionTax, #CapitalGainsTax, #ComprehensiveRealEstateTax, #IncomeTax, #ValueAddedTax, #TaxBenefits, #MultiChildBenefits, #MonthlyRentTaxCredit, #EducationExpensesTaxCredit, #CreditCardIncomeDeduction, #Investment, #FinancialManagement, #Stocks, #LargeShareholders, #MinistryOfEconomyAndFinance, #EconomicPolicy, #LivelihoodStabilization, #RevenueExpansion, #AI, #Semiconductors, #Webtoon, #KContent, #SupportForSmallBusinesses, #RegionalGiftCertificates, #Pension, #TaxNormalization, #TaxSaving

Frequently Asked Questions (FAQ)

Q. What are the main directions of the 2025 tax reform plan?

The 2025 tax reform plan focuses on three directions: striving towards becoming an economic powerhouse, stabilizing livelihoods, and strengthening the revenue base.

The Ministry of Economy and Finance has prepared the 2025 tax reform plan considering changes in population structure, stagnant productivity, and increased welfare burdens due to aging. The three main policy directions are: strengthening tax support for achieving the goal of becoming an economic powerhouse, alleviating the tax burden for ordinary and middle-class citizens, and expanding the weakened revenue base. This direction is expected to positively impact both the corporate investment environment and household finances.

Q. What are the tax support measures for future strategic industries?

Expanding R&D and investment tax credits for future strategic industries like AI, semiconductors, and K-content.

The government designates strategic technologies such as generative AI and agent AI and will provide a maximum 30% investment tax credit for data center facilities. To attract overseas AI talents, the system for a 50% income tax reduction for ten years will also be extended by three years. In the K-content sector, measures include the introduction of production cost tax credits for webtoon creations and enhanced video production cost tax credit rates, all contributing to strengthening industry competitiveness.

Q. How have tax benefits for multi-child households changed?

The credit card income deduction ceiling has been increased by 500,000 won per child, and the tax-exempt scope for childcare allowances has also expanded.

For employees with a total salary of 70 million won or less, the credit card income deduction limit has been expanded to 500,000 won per child, up to a maximum of 1 million won. The tax-exempt limit for childcare allowances for children under six years old has also changed from a flat monthly rate of 200,000 won to a monthly amount of 200,000 won per child, effectively alleviating the economic burden on multi-child households. This is a measure aimed at reducing actual childcare costs.

Q. What are the measures for expanding tax credits for ordinary and middle-class citizens?

Significant expansion of education expense tax credits for extracurricular activities of elementary school students and broadening of the monthly rent tax credit eligibility.

The tuition fees for extracurricular activities for elementary school students in grades 1 and 2 will now be eligible for education tax credits, allowing a 15% tax credit up to an annual limit of 3 million won. To support housing stability, the eligibility criteria for monthly rent tax credits for households with three or more children have been expanded to include properties up to 100 square meters, contributing to reducing housing cost burdens.

Q. What are the normalization measures for tax burdens such as corporate tax and securities transaction tax?

The corporate tax rate will be increased to 2022 levels, and the securities transaction tax rate and the threshold for large shareholder capital gains tax will revert to earlier standards.

The corporate tax rate will be increased by 1% point up to 25% based on the tax standard and will return to the levels pre-2023 reduction. The KOSPI securities transaction tax rate will be adjusted to 0.05%, and KOSDAQ will rise to 0.20%, with the threshold for capital gains tax on large shareholders being raised to a holding amount of 1 billion won or more. These normalization policies aim to secure fiscal soundness and enhance tax equity.