Table of Contents

- Interpretation of Real Estate, Finance, and Government Policy: The Effectiveness of Strategies Between Protecting Genuine Demand and Market Stability?

- 1. 50% Reduction in Total Management Targets, 25% Reduction in Policy Loans… Selective Supply Focused on Real Demand

- 2. Expansion of Regulations Centered on the Metropolitan Area… “Loans for purposes other than actual residence are effectively blocked”

- 3. Mortgage credit limit set at 600 million won, LTV for first-time home buyers lowered to 70%

- 4. Credit loans also limited to within annual income, measures to block DSR circumvention

- Policy Effect Analysis: Is it Market Contraction or a Soft Landing Induction?

- Conclusion: Early Liquidity Prevention Device for Interest Rate Cuts… Need for Protections for Genuine Demand Buyers

- Frequently Asked Questions (FAQ)

Interpretation of Real Estate, Finance, and Government Policy: The Effectiveness of Strategies Between Protecting Genuine Demand and Market Stability?

Starting from June 28, 2025, the government plans to implement strict loan regulations to curb the increase in household debt.

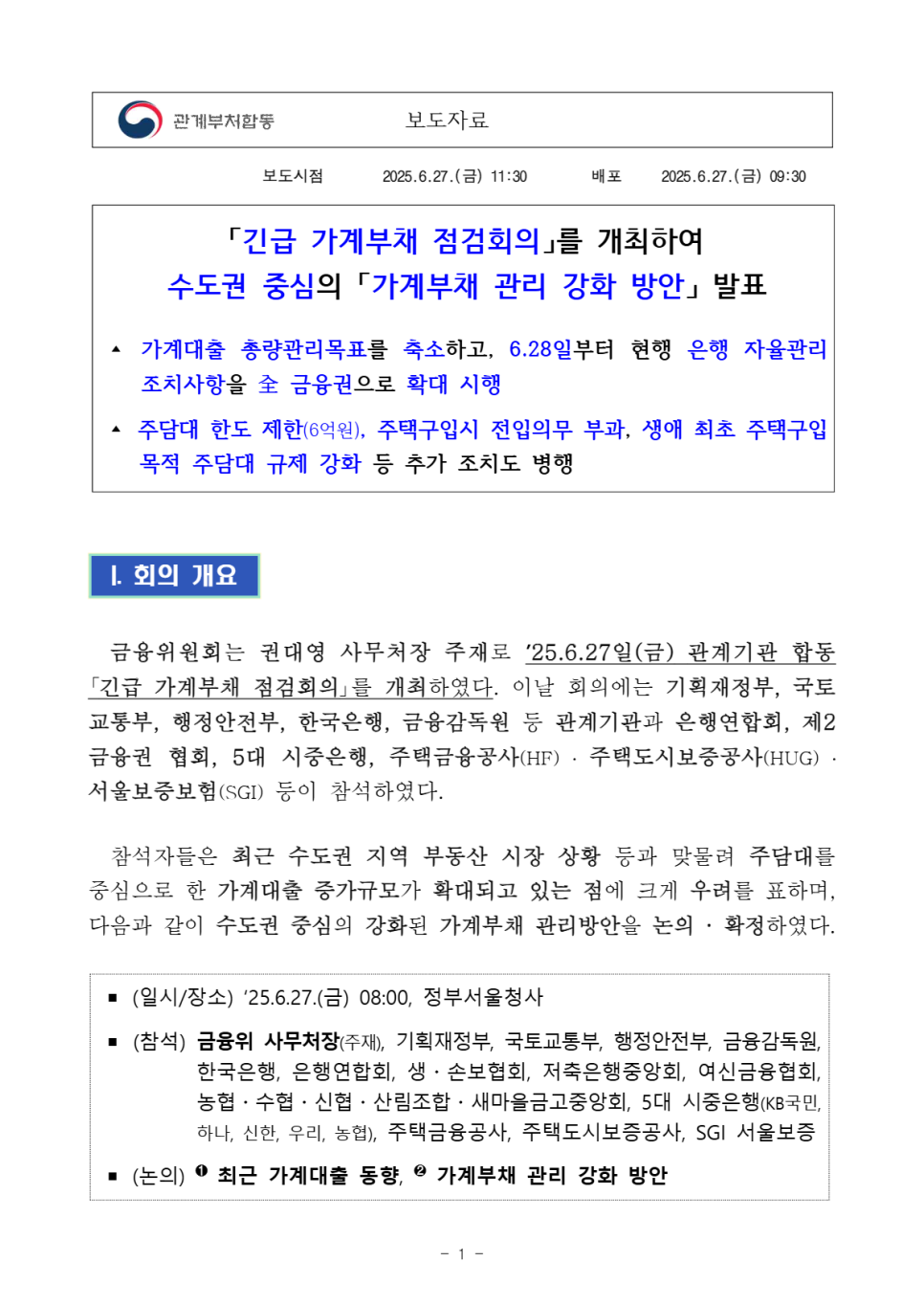

The Financial Services Commission held an "Emergency Household Debt Inspection Meeting" with relevant agencies such as the Ministry of Strategy and Finance and the Ministry of Land, Infrastructure and Transport on June 27, 2025, finalizing and announcing "Strengthening Measures for Household Debt Management" focused on the metropolitan area.

This measure can be interpreted as a warning about the overheating risks in the metropolitan area while reaffirming the policy stance focusing on genuine demand. Through this, the government plans to continue efforts to address the household debt issue.

This policy includes reducing the total loan management target, preventing additional loans for multiple homeowners, and raising the standards for loans to genuine demanders. This is expected to have a significant impact on the market.

The main contents of this policy can be summarized in three points: first, the reduction of total management targets; second, the expansion of regulatory scope to all financial sectors; and finally, the strengthening of limits and conditions for mortgage loans (LTV) and credit loans.

1. 50% Reduction in Total Management Targets, 25% Reduction in Policy Loans… Selective Supply Focused on Real Demand

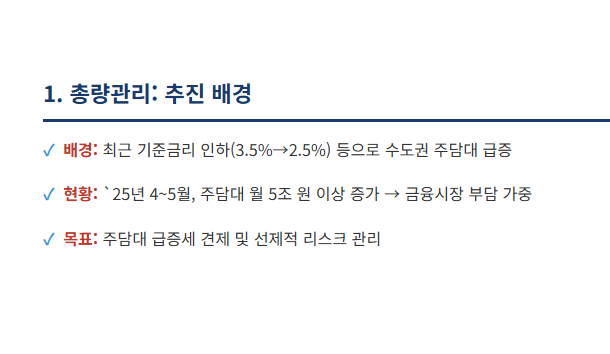

The financial authorities have decided to reduce the supply of household loans by half from the original plan starting in the second half of this year. Additionally, policy loans such as the stepping stone and home subsidy loans will also see a 25% reduction in the annual supply plan. This appears to be a measure aimed at increasing the stability of the financial market.

With the recent decline in the base interest rate from 3.5% to 2.5% and the lifting of the land transaction approval system, measures to curb the increase of mortgage loans in the metropolitan area have become necessary. It is actually expected that mortgage loans will increase by more than 5 trillion won per month between April and May 2025, which could pose a significant burden on the financial market.

2. Expansion of Regulations Centered on the Metropolitan Area… “Loans for purposes other than actual residence are effectively blocked”

The focus of this policy is to effectively curb speculative demand. The government identifies multiple homeowners and gap investors as major causes of increasing household debt and aims to block the flow of funds to these groups. Such measures are intended to enhance market stability.

The most robust countermeasure involves completely banning mortgage loans for purchasing additional homes by existing homeowners and multiple homeowners within the metropolitan and regulated areas. This is a strong measure that effectively makes purchasing additional homes through loans nearly impossible.

Previously, LTV was 30% in regulated areas and 60% in non-regulated areas, but starting June 28, 0% LTV will be applied across the metropolitan area. Additionally, only homeowners who sell their existing homes within six months will be subject to LTV limits equivalent to that of non-homeowners, increasing the burden even temporarily for those who become second homeowners.

This change is expected to have a significant impact on the housing market.

Measures to curb gap investment are being strengthened. In the metropolitan and regulated areas, jeonse loans conditional on ownership transfer are prohibited, blocking the method of using jeonse deposits to pay off the housing balance.

Moreover, by limiting the credit loan limit within the borrower's annual income range, indirect methods of raising funds needed for purchasing homes through credit loans will also be blocked. These measures reflect the strong will of the policy authorities.

When purchasing a home in the metropolitan area, there is now an obligation to move in within six months. Violation of this will result in the full recovery of the loan amount and strict regulations restricting loans for the next three years will be enforced. Particularly, the same regulations will apply to policy loans such as stepping stone loans and home subsidy loans, effectively rendering loans for non-residential purposes impossible. This is expected to have a substantial impact on the housing market.

Mortgage loans for the purpose of living stabilization are set with a maximum limit of 100 million won. Additionally, the term for mortgage loans will be limited to within 30 years. With these new regulations set to be introduced, they are expected to impact the loan market significantly.

3. Mortgage credit limit set at 600 million won, LTV for first-time home buyers lowered to 70%

The recent policy of the government not only aims to curb speculative demand but also brings significant changes for genuine demanders. Notably, the maximum limit for mortgage loans for purchasing homes in the metropolitan area and regulated zones is set at 600 million won.

This measure is intended to prevent excessive high leverage when purchasing high-priced homes, with the actual loan amount being determined within the 600 million won limit based on regulatory rates like LTV and DSR.

As a result, genuine buyers wishing to purchase apartments in popular areas of Seoul and the metropolitan area will have to prepare much more of their own capital. It is essential to pay attention to how this change will impact the housing market in the future.

It is noteworthy that the benefits provided to first-time home buyers have been reduced. Previously, an LTV of 80% was applicable in all areas, but now this rate will be lowered to 70% in the metropolitan and regulated regions. Moreover, a new obligation to move within six months after receiving the loan has been established. This reflects the intent to prevent first-time home buyers from abusing loans to purchase homes and allows only loans for actual residency purposes.

Changes have occurred regarding the limits on policy loans. Most loan types, including stepping stone and support loans, will see a reduction of 20%. This is a measure to align limited resources with the purpose of residential stability for the public, with only the newborn special allowance loan being excluded. These changes impact those who have been receiving policy support and require them to reassess their funding plans.

4. Credit loans also limited to within annual income, measures to block DSR circumvention

This measure is conducted by uniformly limiting the annual income cap per borrower to prevent the circumvention of credit demands through credit loans. Previously, the self-regulation of credit loans could vary within 1-2 times the annual income depending on the financial institution, but now a uniform standard will be applied across all financial sectors.

Additionally, as a measure to block circumvention of DSR regulations, the maturity of mortgage loans will be limited to within 30 years. Furthermore, the guarantee ratio for jeonse loans will be adjusted from 90% to 80% in the metropolitan area. Consequently, banks, insurance companies, and savings banks will have no choice but to strengthen loan screenings, and the growth rate of household loans is expected to drop to single digits in the low to mid teens for the time being.

Policy Effect Analysis: Is it Market Contraction or a Soft Landing Induction?

These measures are expected to play a positive role in curbing the overheating of the real estate market and preventing system risks in the financial market. Particularly, the reinforcement of controls over high-priced homes and investment loans, as well as the clear distinction of regulations focused on genuine demand, shows consistency with the goals of financial policy.

In particular, the six-month move-in obligation serves to institutionally block speculative demand, and the loan limit set at 600 million won suppresses leverage demands targeting high-priced apartments. These measures will contribute to the stability of the market.

However, in the short term, there is a significant likelihood of a sharp drop in transactions and deepening wait-and-see sentiment in the metropolitan housing market. The application of 0% LTV, the setting of a 600 million won mortgage limit, and the imposition of move-in obligations are all likely to significantly suppress the purchasing sentiment for homes. Particularly, it seems that the 2030 generation, who rely heavily on loans, and investors considering additional home purchases will exit the market. As a result, the price increase trend in certain areas that had been overheating is expected to clearly slow down.

In major areas of the metropolitan region, transactions are contracting, and the possibility of price adjustments is increasing. At the same time, in non-regulated areas, a balloon effect is emerging, and funding for first-time home buyers and newlyweds is becoming more difficult. These circumstances could also cause confusion in the financial sector, raising concerns about side effects during the implementation of the policy.

To address these issues, the government plans to apply transitional provisions to those who signed sales contracts or completed loan applications before the implementation of the system. Furthermore, financial institutions are advised to operate exceptional reviews for genuine demanders, the underprivileged, and vulnerable groups. There is a need for efforts to enhance the effectiveness of the policy and secure market stability through these measures.

Conclusion: Early Liquidity Prevention Device for Interest Rate Cuts… Need for Protections for Genuine Demand Buyers

The recently announced household debt management measures are gaining attention as a proactive response to the changes in Korea's low-interest environment. They aim to preserve the protection of genuine demanders while incorporating a strong intention to block speculative demand and system risks. This is interpreted as an important measure for maintaining a stable financial environment in the future.

The financial authorities have decided to hold weekly household debt inspection meetings in the future. In these meetings, additional regulatory measures such as further strengthening LTV, expanding DSR, and adjusting the risk weight of mortgage loans will also be discussed. As the government pushes for structural responses and field checks simultaneously, the effectiveness of the policy will heavily depend on the swift implementation by the market and financial sector.

#householddebt, #realestatematters, #homemortgageloans, #LTVregulations, #DSR, #FinancialServicesCommission, #realestatepolicy, #metropolitanrealestate, #apartments, #housingmarket, #gapinvestment, #multiplehomeowners, #firsttimebuyers, #steppingstoneloans, #supportloans, #jeonseloans, #creditloans, #realestateoutlook, #assetmanagement, #investment, #financialnews, #economicpolicy, #governmentannouncement, #emergencyhouseholddebtinspectionmeeting, #realestateguidelines, #housing_supply, #homeownership, #realestateinvestment, #softlanding, #interestratereduction

Frequently Asked Questions (FAQ)

Q. What are the main contents of the household debt regulations starting from June 28, 2025?

The government will implement a reduction in total management targets, stricter loan limits in regulated areas, and reduction of mortgage and credit loan limits.

From June 28, 2025, in order to curb household debt, the total management target will be reduced by 50%, and policy loans will be decreased by 25%. In the metropolitan area and regulated regions, mortgage loans (LTV) will be capped at 0%, and additional mortgage loans for multiple homeowners will be banned. Additionally, credit loans will be limited to within annual income, among other measures that strictly strengthen loan conditions and limits.

Q. What impact will the strengthened mortgage loan regulations in the metropolitan area have on the market?

The regulations are expected to constrict housing transactions in the metropolitan area and significantly reduce investment demand.

The application of 0% LTV in the metropolitan area, the setting of a maximum mortgage limit of 600 million won, and the imposition of a six-month move-in obligation will likely suppress housing purchasing sentiment, leading to a decrease in transaction volume and a cautious market outlook. In particular, it seems that the 2030 generation, who relies heavily on loans, as well as investors considering additional home purchases, will exit the market. Consequently, price increases in certain overheated areas are expected to slow down. However, there could also be a balloon effect in non-regulated areas.

Q. What policy measures are in place to protect genuine demanders?

There are protection measures such as easing limits and conditions for genuine demand loans and recommending exceptional applications.

The government aims to protect genuine demanders by applying transitional provisions for those who have signed sales contracts or completed loan applications, and it also recommends financial institutions to operate exceptional review processes for low-income and vulnerable groups. Although the LTV for first-time home buyers has been reduced to 70%, a direction has been maintained such that only loans for actual residency purposes will be allowed to clarify the distinction between speculation and genuine demand.

Q. What are the government's additional plans for strengthening household debt management?

Weekly inspection meetings will be held to discuss additional measures for strengthening LTV and DSR and managing the risks of mortgage loans.

The financial authorities have decided to institutionalize household debt inspection meetings to continually review additional regulatory measures such as enhancing LTV, expanding DSR regulations, and adjusting the risk weight of mortgage loans. The effectiveness of the policy will heavily rely on the swift implementation by the market and financial sector, which is regarded as a structural response for stabilizing the real estate market and mitigating risks in the financial system.