Table of Contents

Need for Tax Savings through Brokerage ISA

2025 is remembered as a year of significant profit increase. By investing in various assets such as leveraged ETFs, inverse ETFs, US stocks, and commodities, a large portion of annual income has reached the bracket where a dividend income tax rate of 15.4% applies.

The problem is that if financial income from dividends or distributions exceeds 20 million won, the tax burden may increase dramatically due to comprehensive taxation on financial income. For this reason, the brokerage ISA account has become the best choice, as it allows for efficient tax management.

I plan to open a new account in December and deposit 20 million won immediately. Then, I will add another 20 million won in the first half of 2026, aiming to maximize the available operating amount of 40 million won.

Structure of ISA Tax Benefits

The tax-saving strategy of the ISA can be summarized in four elements: tax exemption, separate taxation, profit and loss offset, and tax deferral. The most prominent advantage of this account is the ability to simultaneously enjoy various tax benefits. It is advisable to think of it as an account designed with favorable tax mechanisms rather than just one that imposes lower taxes.

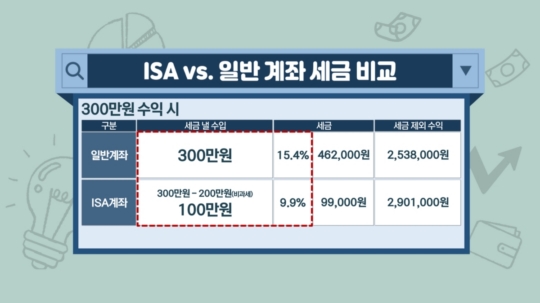

The tax exemption limit varies based on net income. For the general type, the tax exemption limit is 2 million won, while for the low-income or farmer type, it can go up to 4 million won if conditions are met.

Any amount exceeding the tax-free limit is subject to a separate taxation rate of 9.9%. This structure reduces the tax burden compared to the 15.4% rate applied to dividend income in general accounts.

Profit and loss offset allows for the taxation of only the final net profit by aggregating the profits and losses of each account. For instance, if an A account reports a profit of 3 million won while a B account incurs a loss of 1 million won, the final net profit would be 2 million won. If this falls within the tax-free limit, no tax is levied.

Furthermore, tax deferral allows for the taxation not to occur immediately but to be settled at maturity or termination. This structure means that the money that would have gone out for taxes remains in the account and can be reinvested, providing a long-term compounding benefit.

Taxation Issues with ETFs and Dividend Income Tax

The importance of the ISA for active ETF traders lies in its tax structure rather than the frequency of transactions. Understanding taxation is essential for those who frequently buy and sell ETFs. It is important to note that not all domestic ETFs listed in Korea are exempt from taxes.

First, trading profits from domestic individual stocks and domestic equity ETFs are treated as tax-free. However, dividends incur a 15.4% dividend income tax, requiring caution.

On the other hand, for overseas equity, derivatives, bonds, and commodity ETFs listed in Korea, the situation is different. These ETFs face 15.4% withholding tax not only on trading profits but also on distributions. Therefore, when trading growth-oriented overseas ETFs in Korea, it is important to be aware of the cumulative tax burden in general accounts.

Furthermore, when directly investing in US stocks, the taxation system develops differently. Capital gains are exempt from taxation up to 2.5 million won per year, with a 22% capital gains tax imposed on amounts exceeding this limit. The dividend income tax rate of 15.4% applies, making it crucial to understand this tax framework and formulate investment strategies accordingly.

Ultimately, tax issues in ETF investments cannot be overlooked, so investors must establish strategies based on a clear understanding.

Amidst this flow, actively managing ETFs in general accounts may increase tax burdens on dividends and distributions, thereby raising the risk of comprehensive taxation on financial income. Therefore, for those frequently trading ETFs, considering the ISA account as a "tax-saving-only account" would be advisable.

Changes in ISA Tax Law for 2025

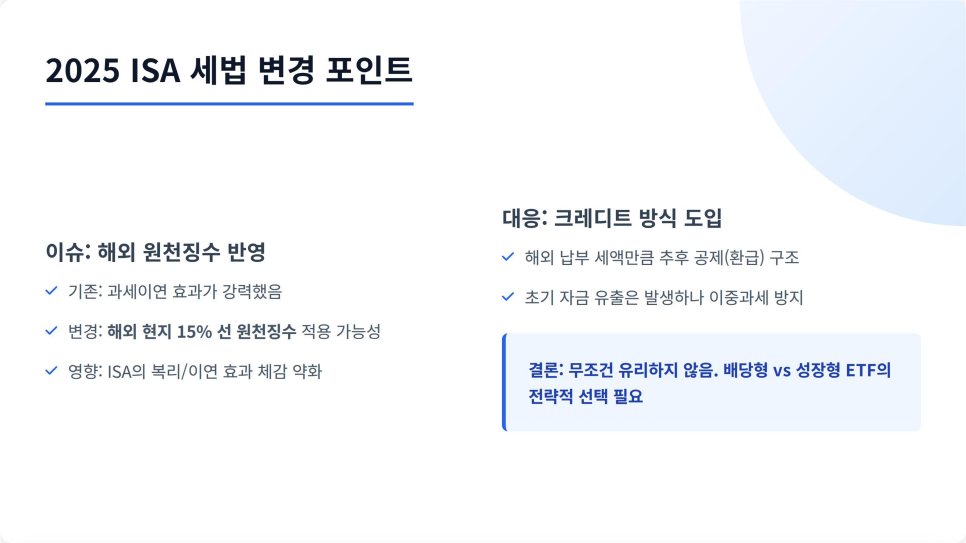

The central change to take place in 2025 is that "the structure will apply taxes withheld overseas on dividends from overseas ETFs listed in Korea, resulting in a reduction of the tax deferral effect on dividends within the ISA."

After the deferral period ends, about 15% tax will be withheld by the U.S. This has raised concerns that the anticipated tax deferral and compounding effects through the ISA may be diminished. To address this, the government is developing a credit system to allow a deduction of some of the taxes withheld overseas when applying for ISA taxation.

However, since initial withholding will still be maintained, there is now a perception that the actual tax burden has increased compared to before.

Ultimately, after 2025, the simple formula that states "using an ISA is always advantageous for overseas dividends" will no longer hold. Therefore, careful and strategic decisions will need to be made about which ETFs to include in the ISA (between dividend-based and capital gain-based strategies).

Brokerage ISA Operation Strategy

In 2025, I felt the burden of dividend income tax as profits increased. Consequently, I decided to adjust my asset structure more efficiently in 2026.

Specifically, the following aspects are important. First, the annual contribution limit is 20 million won, and it is necessary to allocate funds within a total limit of 100 million won over five years. Considering the mandatory holding period of three years, it is advisable to operate with "planned investment funds" rather than short-term funds.

I will open the account in December to secure the annual limit and then make additional contributions in January of the following year to expand the operational scale. Since aggressive ETF management may erode returns through taxes, if the separate taxation rate stays at around 10% (9.9%), I believe it is worth attempting.

The goal for 2026 is not just to increase profits. The core is to pursue stable asset growth centered on after-tax returns. Even if the same profit is achieved, the range of future investment opportunities can change significantly depending on tax savings.

#BrokerageISA, #ISAaccount, #ISA tax saving, #ETF taxation, #dividend income tax, #comprehensive taxation of financial income, #separate taxation, #tax-free 2 million won, #annual contribution limit 20 million won, #profit and loss offset, #tax deferral, #after-tax return, #ETF investment, #leveraged ETF, #inverse ETF, #US stock investment, #commodity investment, #overseas ETF, #domestic listed ETF, #dividend ETF, #growth ETF, #S, #&P500 ETF, #NASDAQ ETF, #retirement account transfer, #maturity strategy, #tax saving strategy, #investment account management, #asset management, #tax management, #2026 investment strategy

Frequently Asked Questions (FAQ)

Q. What is the reason for needing tax savings through the brokerage ISA account?

The brokerage ISA account is the best way to reduce the burdens of dividend income tax and comprehensive taxation on financial income.

As investment profits increased significantly in 2025, many have reached the range where a 15.4% dividend income tax applies. Especially if financial income exceeds 20 million won annually, the tax burden can surge due to the comprehensive taxation on financial income, necessitating efficient tax management. The brokerage ISA account is the optimal account that reduces these tax burdens and allows for various tax-saving benefits.

Q. How is the structure of ISA tax-saving benefits?

ISA provides four tax benefits: tax exemption, separate taxation, profit and loss offset, and tax deferral.

The tax exemption limit varies based on net income, with the general type being 2 million won and up to 4 million won for low-income and farmer types if conditions are met. Income exceeding the tax exemption limit is subject to a separate taxation rate of 9.9%, which is lower than the 15.4% applied in general accounts. In addition, various account profit and loss offsets apply taxation only on net profit and defer taxes, allowing the compounding effect by postponing the payment of taxes to maturity or termination.

Q. What are the main changes in ISA tax law for 2025?

From 2025, overseas withholding taxes will apply to dividends from overseas-listed ETFs, reducing the tax deferral effect of ISA.

Approximately 15% tax will be withheld overseas on dividends from domestic-listed overseas ETFs, raising concerns about the reduction of tax deferral and compounding effects through the ISA. The government is introducing a credit system that allows partial deductions of overseas withholding taxes during ISA taxation, but initial withholdings remain, increasing the actual tax burden compared to previous levels. Therefore, after 2025, simply expecting tax-saving effects on overseas ETF dividends from ISA utilization will require more careful strategy formulation.

Q. What advantages does an ISA account offer when investing in ETFs?

The ISA account is advantageous for reducing tax burdens, such as benefiting from tax-free trading profits and lower dividend income tax when trading ETFs.

While trading profits from domestic stocks and domestic equity ETFs are tax-free, a 15.4% dividend income tax applies to dividend income. Particularly, for overseas equity, derivatives, bonds, and commodity ETFs, both trading profits and distributions are subject to the 15.4% dividend income tax, potentially increasing tax burdens in general accounts. The ISA account improves this tax structure, reducing tax burdens and providing separate taxation benefits with lower dividend tax rates, contributing to increased investment returns.

Q. How should I plan the operation strategy for my brokerage ISA account?

You should focus on planned, long-term investments and tax savings within the annual 20 million won contribution limit.

The ISA account, which allows an annual contribution of 20 million won and a maximum of 100 million won over five years, is suitable for long-term investments requiring a mandatory holding period of at least three years. It is more stable to operate with planned investment funds rather than short-term funds. Opening the account in December and depositing funds to secure the annual limit, and then increasing the operational scale with additional contributions the following year is an effective strategy. Even in aggressive ETF investments, it’s important to maximize after-tax returns considering the ISA's 9.9% separate taxation benefits.