Table of Contents

- The 'Complex Crisis' of the Korean Financial Market in Q4 2025

- The Dilemma of BOK and Fed: The Fog of Monetary Policy

- The Arrival of 6% Mortgage Rates and the Background of the 1,460 Won Exchange Rate

- Investment Strategies Compared to the First Half of 2026: Real Estate and Stocks

- Conclusion: Asset Reallocation Strategies Amid the Complex Crisis

- Frequently Asked Questions (FAQ)

The 'Complex Crisis' of the Korean Financial Market in Q4 2025

In the third week of November 2025, the financial environment in Korea is revealing the onset of a 'polycrisis'.

This situation arises from the intricate interplay of five key factors: the Bank of Korea's monetary policy, mortgage interest rates, the interest rate differential between Korea and the U.S., the won to dollar exchange rate, and M2 liquidity, which compound the risks.

The interaction of these elements underscores the current instability in the financial markets.

The mortgage interest rate has surpassed 6% for the first time in two years. Additionally, the won/dollar exchange rate has surged to 1,460 won, significantly impacting the real economy and asset markets. This change is expected to impose a severe financial burden on many.

This time, we will examine the various factors that will affect the asset market until the first half of 2026 and propose effective investment strategies.

The Dilemma of BOK and Fed: The Fog of Monetary Policy

The current market turmoil stems from uncertainty regarding monetary policy. The likelihood of a Fed rate cut in December has dropped to 40%, reiterating the 'Higher for Longer' stance. This situation acts as a factor that undermines expectations of reduced interest rate differentials between Korea and the United States and leads to a strong dollar.

The Bank of Korea currently faces a complex situation. Due to the strong remarks of Governor Lee Chang-yong, market expectations for interest rate cuts have swiftly shifted to concerns about rate hikes. This scenario illustrates the conflict between two factors: slowing economic growth and high exchange rates and rising prices.

In fact, as the possibility of rate hikes is mentioned, 'verbal intervention' has been conducted to manage household debt and defend against won depreciation. However, these measures are causing a surge in market interest rates as a side effect.

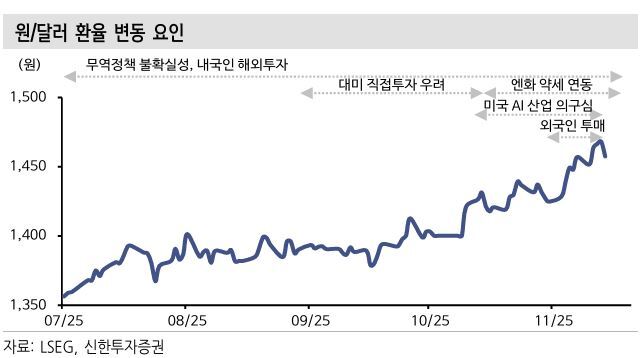

The Arrival of 6% Mortgage Rates and the Background of the 1,460 Won Exchange Rate

Despite the Bank of Korea's unchanged base rate, the ceiling on mortgage interest rates has exceeded 6%. This is influenced by comments from the Bank's Governor, leading to a sharp rise in the benchmark bank bond rates and banks raising their margins, resulting in decreased loan accessibility.

The 6% rate affects the DSR limits for new borrowers. Furthermore, for existing borrowers who took out loans at around 2% in 2020 and 2021, the interest burden is set to surge, which may further accelerate the contraction of private consumption.

Meanwhile, the reason for the exchange rate surging to the 1,460 won level is primarily due to the net selling of over 7 trillion won in foreign stocks.

"However, this exchange rate surge is more significantly affected by the 'loss of defense' that needs to be countered rather than the volume of sell orders that flowed in."

The limited intervention by foreign exchange authorities and large corporations delaying dollar sales are structurally causing 'overshooting' phenomena.

Investment Strategies Compared to the First Half of 2026: Real Estate and Stocks

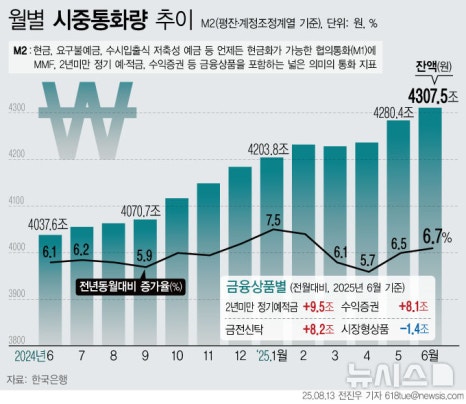

Paradoxically, despite the high rates of nearly 6%, the M2 broad money supply is experiencing an 8.5% increase in liquidity. This indicates that much of the capital is trapped in short-term accounts due to a lack of appropriate investment opportunities. This liquidity could act as a potential factor for sharp volatility when uncertainties surrounding policies are resolved in the future.

The 'sale (wait-and-see)' and 'jeonse (rise)' flows are showing completely different trends in the real estate market. The burden of high rates around 6% could lead to a sharp decrease in transaction volume in the sales market, but as purchasing demand shifts to jeonse, prices continue to rise.

The stock market faces a very unfavorable situation due to foreign capital outflows and concerns over the AI bubble adjustment. This is imposing a significant burden on investors.

Conclusion: Asset Reallocation Strategies Amid the Complex Crisis

In November 2025, the Korean economy is experiencing a complex crisis defined by 'high interest rates, high exchange rates, and low growth.' It is an ironic situation where M2 liquidity is increasing amidst policy uncertainties.

In the current economic situation, investors need to readjust their portfolios. There are three strategies to consider.

First, it is important to reduce debt or switch to fixed-rate loans to adequately respond to effective rates around 6%. Second, as the risks associated with 100% won-denominated assets become clear, about 30% of the portfolio should be diversified into 'dollar assets,' meaning high-quality U.S. stocks.

Lastly, securing liquidity is essential. It is necessary to hold assets in dollars or ultra-short-term bonds instead of won, preparing for the time when policy uncertainties are resolved as 'ammunition.' By utilizing these methods, a stable investment environment can be created.

#Mortgage6, #%, #ExchangeRate1460Won, #2025EconomicOutlook, #BankofKorea, #InterestRateHike, #ComplexCrisis, #AssetAllocationStrategy, #InvestmentStrategy, #RealEstateMarket, #StockMarket, #KOSPI, #FederalReserve, #FOMC, #KoreanUSInterestRateGap, #M2Liquidity, #ForeignCapitalOutflow, #WonDollarExchangeRate, #EconomicCrisis, #MortgageInterestRates, #LeeChangYong, #Hawkish, #RealEstateOutlook, #JeonseRate, #DomesticRecession, #Stagflation, #DollarAssets, #USStocks, #WealthManagement, #EconomicInsights, #FinancialMarket

Frequently Asked Questions (FAQ)

Q. What is the reason for the complex crisis facing the Korean financial market in Q4 2025?

The Bank of Korea's monetary policy, mortgage rates, the Korean-US interest rate differential, exchange rates, and M2 liquidity collectively heighten financial instability.

As of November 2025, the Korean financial market has entered a "complex crisis" due to the intertwining of five elements: the Bank of Korea's monetary policy, rising mortgage interest rates, the interest rate differential between Korea and the U.S., the sharp rise in the won to dollar exchange rate, and increasing M2 liquidity. These factors are influencing one another, spreading instability in the financial markets. Notably, interest rate hikes and rising exchange rates are placing additional burdens on the real economy and asset markets.

Q. What are the background and impacts of mortgage rates surpassing 6%?

Rising bank bond rates and increasing margins from banks have led mortgage rates to surpass 6%, significantly increasing borrower burden.

Although the base rate remains unchanged, comments from the Bank of Korea's Governor regarding the possibility of interest rate hikes have caused the benchmark bank bond rates to spike, leading banks to increase their lending margins and pushing mortgage rates above 6% for the first time in two years. As a result, the DSR limit for new borrowers is being lowered, while existing borrowers face a significant increase in interest burdens, leading to a contraction in private consumption. This can pose serious financial burdens not only on the financial market but also on the real economy.

Q. What caused the won/dollar exchange rate to surge to 1,460 won?

Net selling of foreign stocks, limited intervention from foreign exchange authorities, and delays in dollar sales by corporations have propelled the surge in the exchange rate.

The primary reason for the sharp increase in the exchange rate is the net selling of over 7 trillion won in foreign stocks. Additionally, the limited intervention by foreign exchange authorities and delays in dollar sales by major corporations have led to structural 'overshooting' phenomena in the market. This situation continues to exert depreciation pressure on the won, worsening the uncertainty not only in the real economy but also in the financial markets.

Q. What investment strategies are suggested in comparison to the first half of 2026?

It is recommended to reduce debt, diversify 30% into dollar assets, and secure liquidity for stable asset management.

First, it is important to reduce debt or convert to fixed-rate loans to adequately respond to effective rates around 6%. Second, as the risks associated with won-denominated assets have become clearer, about 30% of the portfolio should be diversified into dollar assets such as high-quality U.S. stocks. Third, it’s necessary to secure liquidity in the form of dollars or ultra-short-term bonds rather than won to prepare 'ammunition' for the time when policy uncertainties are resolved. With these strategies, risks can be minimized in the uncertain asset market environment.

Q. What impact do the monetary policies of the Bank of Korea and the Federal Reserve have on the financial market?

Fears of interest rate hikes by the BOK and reduced likelihood of rate cuts by the Fed undermine expectations of narrowing interest rate differentials and lead to a stronger dollar.

The possibility of a Fed rate cut in December has declined to 40%, highlighting the 'Higher for Longer' policy stance. As a result, expectations for narrowing interest rate differentials between Korea and the U.S. have been dashed, leading to a strengthened dollar. Conversely, the Bank of Korea is hinting at possible rate hikes amid the conflict of slowing economic growth and high exchange rates and inflation, while also employing verbal interventions to manage household debt. These uncertainties in monetary policy are key factors amplifying volatility in the financial markets.