Table of Contents

- Turning Point in the Secondary Battery Industry: A New Investment Map is Needed

- Beyond the Electric Vehicle Chasm, ESS Rises as the New Heart

- Intensified Technical Hegemony Competition: The Counterattack of LFP and the Response of K-Batteries

- Geopolitical Risks: Opportunities and Threats in the 'Golden Cage' of IRA

- Investment in Leveraged ETFs in the Secondary Battery Market: In-Depth Comparison of KODEX vs TIGER

- Conclusion: Deciding Market Entry with TIGER Secondary Battery TOP10 Leveraged Dollar-Cost Averaging

- Frequently Asked Questions (FAQ)

Turning Point in the Secondary Battery Industry: A New Investment Map is Needed

The global secondary battery industry is at an important turning point. While there is a notable decrease in short-term demand in the electric vehicle (EV) market, highlighted by the phenomenon known as the 'Chasm', the rise of energy storage systems (ESS) is strengthening the foundation of the industry. As a new growth driver, ESS is brightening the future of this sector.

It is now time to move beyond analysis limited to the past growth of electric vehicles and to consider various forms of demand, technological competition, and geopolitical factors comprehensively. It is crucial to understand these complex elements and establish a new investment direction.

This article will analyze the current status of the secondary battery industry and provide a detailed comparison of the prominent leveraged ETFs, KODEX and TIGER. Through this, I aim to propose a more effective investment strategy.

Beyond the Electric Vehicle Chasm, ESS Rises as the New Heart

Diverging Electric Vehicle Markets: Slowdown in North America and Growth in Europe

It is clear that the growth rate in the electric vehicle market is slowing down. Particularly in North America, concerns about declining demand arise as consumer tax credit benefits due to the U.S. Inflation Reduction Act (IRA) are set to expire soon. In fact, by the first half of 2025, the growth rate of electric vehicle sales in North America is expected to be only 3%, indicating a significant slowdown in growth.

However, not all regions are showing the same trend. The European market is maintaining a stable growth trend, driven by strong CO₂ regulations, which are expected to induce an annual sales growth of approximately 20% until 2027. These policies are expected to influence the future direction of the electric vehicle market.

A New Growth Driver for the Industry: The Explosion of the ESS Market

The energy storage system (ESS) market plays a crucial role in a volatile market. The U.S. ESS market has tripled in the past three years, with an estimated additional growth of about 34% expected by 2025. This trend is contributing to its establishment as a new center for the industry.

The current growth of the secondary battery industry is closely related to the spread of renewable energy sources such as solar and wind, as well as the high power consumption of AI data centers. Large corporations like Microsoft and Google are investing heavily in energy storage systems (ESS) to achieve carbon neutrality, which has the potential to generate more consistent demand in the secondary battery field than in the automobile market.

In this way, the secondary battery industry is no longer limited to electric vehicles, but is strengthening its foundation through new drivers such as AI infrastructure and renewable energy. These changes are positively impacting the entire industry, indicating greater growth potential in the future.

Intensified Technical Hegemony Competition: The Counterattack of LFP and the Response of K-Batteries

The Rise of LFP Batteries and the Strategic Shift of K-Batteries

Currently, the technological competition in the secondary battery industry is framed around the battle between Korea's NCM (Nickel Cobalt Manganese) batteries and China's Lithium Iron Phosphate (LFP) batteries. LFP batteries are cheaper, safer, and have improved energy density from past disadvantages, causing significant changes in the market.

In 2020, the market share of LFP was only 17%, but it is expected to increase to 47% by 2026. Especially in the energy storage system (ESS) market, where cost competitiveness is crucial, LFP has emerged as the most attractive option. Thus, LFP batteries appear set to play an important role in the future market.

Recently, in response to market changes, the three Korean battery manufacturers that have traditionally focused on NCM batteries are also adopting LFP technology for survival. LG Energy Solution has begun mass production of LFP batteries exclusively for ESS at its Arizona plant, and recently signed a large-scale supply contract worth 6 trillion won with a customer related to Tesla for three years, demonstrating aggressive moves.

Samsung SDI and SK On are also focusing their efforts on developing LFP batteries to target the mid-range electric vehicle and ESS markets. In this way, the domestic battery industry is actively adopting various technologies to enhance competitiveness.

Competition for the Future: Solid-State Batteries

Solid-state batteries are gaining attention as a technology that will lead to innovative changes in the market in the long term. Samsung SDI is operating a pilot line aiming for commercialization by 2027 and securing technological advantages.

The solid-state battery market is expected to reach 40 billion dollars by 2030, making it a crucial factor for competitive strength in the future market.

Geopolitical Risks: Opportunities and Threats in the 'Golden Cage' of IRA

The Dual Nature of the US IRA: Opportunities and 'Trump Risk'

The secondary battery industry can no longer be explained solely by economic principles. The US Inflation Reduction Act (IRA) has become an important variable. According to the IRA's 'Foreign Entity Ownership Criteria (FEOC)', electric vehicles that use battery parts or materials from China are excluded from tax credits.

This opens up new opportunities for Korean companies to gain a foothold in the North American market. This change is expected to positively impact Korea's secondary battery industry.

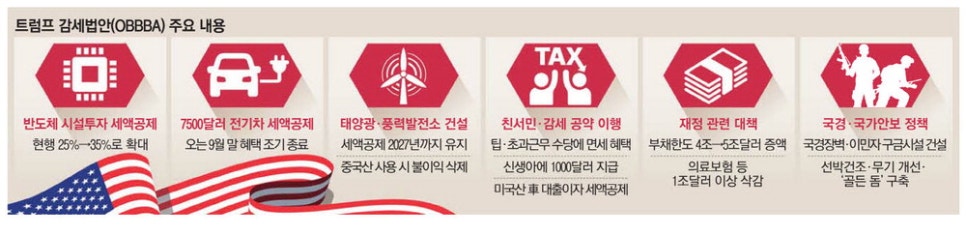

This opportunity comes with significant uncertainties encapsulated in the term 'Trump Risk'. In July 2025, the Trump administration passed a massive tax reduction bill titled the 'One Big Beautiful Bill Act'. This bill primarily aims to abolish numerous clean energy support policies grounded in the Biden administration's Inflation Reduction Act (IRA).

This change could have significant impacts on economic and environmental policies, and market responses must be carefully monitored. Predicting how future policy directions will be set is crucial, and investors need to develop strategies considering these uncertainties.

As of September 30, 2025, tax credits (up to $7,500) for electric vehicle purchases are set to expire early. Originally planned to last until the end of 2032, if the main provisions of the IRA are modified or abolished, the economic viability of the production facilities invested in by Korean companies in the U.S. may significantly decline.

This raises the risk of these heavily invested facilities turning into 'stranded assets'. Ultimately, the IRA acts as a 'golden cage' for Korean battery companies, ensuring current profits while risking survival due to changes in the political environment.

This situation is expected to pose serious challenges to companies and significantly impact future investment strategies.

Europe's Defensive Strategy: CRMA and Tariff Barriers

The European Union (EU) is protecting its domestic industry and internalizing its supply chain through the Critical Raw Materials Act (CRMA) and imposing high tariffs on Chinese electric vehicles. This global geopolitical environment is expected to significantly influence the future development of K-batteries.

Investment in Leveraged ETFs in the Secondary Battery Market: In-Depth Comparison of KODEX vs TIGER

Essential Considerations Before Investing in Leveraged ETFs

When looking to invest in the growth potential of the secondary battery industry, leveraged ETFs are attracting attention. However, it is essential to fully understand the structural risks of these products before using them. Leveraged ETFs are high-risk products designed to double the daily returns of their underlying index. In environments where the market is fluctuating without a clear direction, there is a significant risk of losing principal.

In particular, these products can lead to losses during long holding periods due to the 'negative compounding effect'. Therefore, leveraged products should not be viewed as a 'buy and hold' strategy based on continuous growth of the industry, but rather as tactical trading tools that require confidence in short-term market direction. Investment decisions should be made after considering these aspects thoroughly.

Fees vs. Investment Philosophy: Key Differences Between TIGER and KODEX

The two important products in the domestic market are KODEX Secondary Battery Industry Leverage (462330) and TIGER Secondary Battery TOP10 Leverage (412570).

The main differences between these two products lie in the index they track and their fee structures.

Fees

The annual total fee for TIGER ETFs is 0.29%, which is significantly lower than KODEX's 0.49%. This reflects intense competition among management companies, providing a real advantage to investors.

| Category | KODEX Secondary Battery Industry Leverage | TIGER Secondary Battery TOP10 Leverage |

| Stock Code | 462330 | 412570 |

| Management Company | Samsung Asset Management | Mirae Asset Management |

| Underlying Index | FnGuide Secondary Battery Industry Index | KRX Secondary Battery TOP10 Index |

| Total Fee (Annual) | 0.49% | 0.29% |

| Net Asset Total | About 287 billion Won | About 55.7 billion Won |

| Core Features | A wide range of stocks across the entire value chain | Focus on the top 10 large-cap stocks |

Investment Philosophy (Underlying Index)

More important than low fees is the difference in investment philosophy.

KODEX Secondary Battery Industry Leverage is managed based on the 'FnGuide Secondary Battery Industry Index'. This index includes about 25 diverse stocks, incorporating cells and materials as well as parts and equipment companies.

This achieves a 'broad diversification' strategy aimed at pursuing growth across the entire industrial ecosystem. The top 10 constituent assets of KODEX Secondary Battery Industry Leverage (462330) reflect this direction well.

| Rank | Holding Stock Name | Stock Code | Weight (%) |

| 1 | KODEX Secondary Battery Industry | 305720 | 14.15 |

| 2 | LG Energy Solution | 373220 | 8.33 |

| 3 | POSCO Holdings | 005490 | 8.24 |

| 4 | EcoPro | 086520 | 6.46 |

| 5 | SK Innovation | 096770 | 5.96 |

| 6 | LG Chem | 051910 | 5.57 |

| 7 | 2025-05 SK Innovation Individual Futures | KR4141W50007 | 4.62 |

| 8 | 2025-05 Samsung SDI Individual Futures | KR4122W50007 | 4.58 |

| 9 | 2025-05 LG Chem Individual Futures | KR4147W50004 | 4.55 |

| 10 | 2025-05 POSCO Holdings Individual Futures | KR4113W50006 | 4.48 |

The TIGER Secondary Battery TOP10 Leveraged ETF follows the 'KRX Secondary Battery TOP10 Index'. This ETF invests in the top 10 largest companies by market capitalization, applying a 'focus and concentration' strategy, assigning 75% of its weight to the top three companies: LG Energy Solution, POSCO Holdings, and SK Innovation.

This approach is based on the anticipation that a few large corporations will have stronger market dominance. The TIGER Secondary Battery TOP10 Leverage (412570) is considered an attractive option for investors as it seeks higher returns by concentrating on specific assets.

| Rank | Holding Stock Name | Stock Code | Weight (%) |

| 1 | Sector Index Secondary Battery TOP 10 F 202509 | KR41ADW90001 | 111.62 |

| 2 | TIGER Secondary Battery TOP10 | 364980 | 22.21 |

| 3 | LG Energy Solution | 373220 | 20.20 |

| 4 | POSCO Holdings | 005490 | 16.12 |

| 5 | SK Innovation | 096770 | 13.16 |

| 6 | LG Chem | 051910 | 5.19 |

| 7 | Samsung SDI | 006400 | 4.17 |

| 8 | EcoPro BM | 247540 | 2.52 |

| 9 | EcoPro | 086520 | 2.32 |

| 10 | POSCO Future M | 003670 | 1.96 |

Conclusion: Deciding Market Entry with TIGER Secondary Battery TOP10 Leveraged Dollar-Cost Averaging

The secondary battery industry is undergoing changes through the rapid growth of the electric vehicle market and new energy storage solutions like ESS. While there is sufficient long-term growth potential, geopolitical risk factors and fierce technological competition pose many challenges.

Amidst these complexities, leveraged ETFs in the secondary battery sector are regarded as useful tools for maximizing the growth potential of the industry. However, they also carry high risks, necessitating careful approaches. Therefore, when making investment decisions, it is important to delve into the fundamental question of 'What is the future outlook for this industry?' beyond simple fee comparisons.

After considerable deliberation, I have come to agree that large corporations equipped with capital and economies of scale will account for most of the market value. Therefore, investing in 'TIGER Secondary Battery TOP10 Leverage', which allows for a relatively low-cost concentration on leading players in the industry to maximize profits arising from their market dominance, seems to be a reasonable judgment.

However, given the various political and technological risks discussed earlier, alongside the inherent volatility of leveraged products, investing all funds at once could be risky. Hence, I plan to adopt a 'dollar-cost averaging' strategy over 1-2 weeks to reduce risks associated with market timing and effectively respond to volatility.

This approach will serve as a cautious first step to clearly recognize and manage potential risks while reaping the benefits of long-term industry growth.

#SecondaryBattery, #SecondaryBatteryETF, #SecondaryBatteryOutlook, #ESS, #EnergyStorageDevice, #LFPBattery, #KODEXSecondaryBatteryIndustryLeverage, #TIGERSecondaryBatteryTOP10Leverage, #ETFComparison, #InvestmentStrategy, #ElectricVehicle, #Chasm, #IRA, #InflationReductionAct, #SamsungSDI, #LGEnergySolution, #SKOn, #POSCOHoldings, #EcoPro, #SolidStateBattery, #USPresidentialElection, #TrumpRisk, #Protectionism, #ETFFees, #LeveragedETF, #StockInvestment, #WealthManagement, #GrowthStocks, #TechStocks, #KBattery

Frequently Asked Questions (FAQ)

Q. Why is ESS important in the secondary battery industry?

ESS is a new growth driver for the secondary battery industry due to the spread of renewable energy and AI infrastructure.

The global secondary battery industry is establishing a solid growth foundation amidst slowing electric vehicle demand thanks to the rapid growth of the ESS market. ESS has become a key solution for addressing the high power demand of AI data centers and the proliferation of renewable energy sources like solar and wind. Massive investments from large companies such as Microsoft and Google are driving the increased demand for ESS. Therefore, the secondary battery industry is expanding its growth potential around ESS, not just electric vehicles.

Q. What are the differences between the North American and European electric vehicle markets?

North America is slowing down due to the IRA expiration, while Europe is expected to grow by 20% thanks to CO₂ regulations.

The North American electric vehicle market is at risk of slowing down, with the growth rate for sales expected to be only 3% in the first half of 2025 due to the expiration of consumer tax credits under the U.S. Inflation Reduction Act (IRA). In contrast, Europe is expected to experience an annual growth rate of approximately 20% through 2027 thanks to strong CO₂ emission regulations. This divergence in growth patterns between the two regions distinctly impacts the global secondary battery industry.

Q. What is the background of the rise of LFP batteries and the market outlook?

LFP batteries are inexpensive and safe, rapidly increasing their market share in the ESS and mid-range electric vehicle markets.

LFP batteries are rapidly expanding their foothold in the secondary battery industry due to price competitiveness and improved safety. Market share, which was 17% in 2020, is projected to grow to 47% by 2026, especially becoming a major battery in the ESS market. Korean battery companies are also adopting LFP technology extensively across various products, positioning LFP batteries as one of the critical technologies in the industry for the future.

Q. What are the differences between KODEX and TIGER leveraged ETFs in the secondary battery industry?

KODEX diversifies investments across the entire industry, while TIGER focuses on the top 10 large corporations.

KODEX Secondary Battery Industry Leverage employs a strategy of broadly investing across the domestic secondary battery industry ecosystem, including about 25 stocks. In contrast, TIGER Secondary Battery TOP10 Leverage concentrates its investments in the top 10 companies by market capitalization, directing 75% of its investment to the three largest: LG Energy Solution, POSCO Holdings, and SK Innovation. With a lower fee of 0.29%, TIGER also reduces the cost burden for investors, necessitating choice based on investment philosophy and index tracking method.

Q. What should be noted when investing in leveraged ETFs?

Leveraged ETFs are suitable for short-term directional bets and carry significant loss risks if held long-term.

Leveraged ETFs are high-risk products designed to double the daily returns of their underlying index. If the market is experiencing sharp fluctuations, the long-term holding can lead to significant principal loss due to the 'negative compounding effect'. Therefore, instead of simply betting on the industry’s long-term growth, it is more suitable to trade tactically when there is confidence in short-term market direction. Understanding the structural risks before investing and approaching thoughtfully is necessary.

Q. What impact does the U.S. IRA legislation have on the secondary battery industry?

The IRA excludes components from China, providing opportunities for Korean companies but also carrying political uncertainties.

The U.S. Inflation Reduction Act (IRA) establishes regulations that exclude electric vehicles using battery parts or raw materials from China from tax credits, providing Korean companies with opportunities to gain a foothold in the North American market. However, political changes, such as the potential for 'Trump Risk' in 2025, also present uncertainties. If IRA provisions change, it could significantly degrade the viability of investments in production facilities and raise the risk of stranded assets. Thus, the IRA embodies a dual nature of opportunity and threat, like a 'golden cage'.